Whilst credit cards can be a useful tool, they often come with a range of different fees. Credit card fees can end up costing you a lot of money in the long run. That’s why we’ve put together this helpful guide on how to reduce credit card fees in 5 simple ways.

What is a credit card?

Before we dive into the ways you can reduce credit card fees – let’s start with the basics. What is a credit card? A credit card is a line of revolving credit at a set limit that refreshes periodically, generally each month.

You can use a credit card to make purchases, balance transfers and cash advances. When you take out a credit card, you do so with the condition that you pay back the money that you spent, plus any additional interest. At the very least, you’ll have to make the minimum repayment each month by the due date.

Different types of credit cards

There are many different types of credit cards which all come with their unique benefits and downfalls. One key rule to keep in mind – if you are getting some kind of benefit, such as rewards, low-interest rates or no annual fee, you are often paying for it in another way. This could be through extra fees or higher interest rates. That’s why it’s a good idea to weigh the pros and cons before deciding on which card is right for you.

Here are some of the most common types of credit cards:

- Low-interest credit card – a low-interest credit card, is a card that offers a lower interest rate than normal. However, to offset the lower interest rate, these types of cards often come with a higher annual fee, more restrictions and fewer rewards.

- Balance transfer credit card – A balance transfer credit card allows you to transfer your credit card debt from another credit card to this one. A balance transfer credit card usually comes with lower interest rates or even an interest-free period. This allows you to repay your debt and save paying interest on your other card. However, this card is only beneficial if you can pay it off within the low or interest-free period, otherwise, it could end up costing you more.

- No annual fee credit card – like the name suggests, this kind of credit card doesn’t come with an annual fee, either for a set period or for the life of the card. However, you’ll usually be charged higher interest rates, which could cost you more in the long run.

- Rewards credit card – This kind of credit card gives you some kind of reward when you make purchases, whether it’s frequent flyer points, retail rewards, supermarket rewards, cashback deals, and petrol rewards.

Common credit card fees

There are several different credit card fees that you’ll need to keep an eye out for. What fees you’ll be charged, and how much they’ll cost you, completely depend on your specific card. That’s why it’s important to read the terms and conditions carefully before applying for a credit card.

Here’s a breakdown of some of the most common credit card fees.

| Annual Fees | Most credit cards come with an annual fee which you’ll be charged each year. The cost of this fee will vary depending on which credit card you have. |

| Interest | Just like an annual fee, most credit cards come with interest. You will be charged interest when you carry a balance (when you don’t completely pay off your credit card debt for the month).

There are different types of interest rates. They might be called: purchase rate, cash advance rate, balance transfer rate or promotional interest rate. |

| Balance transfer fee | A balance transfer is when you move your existing debt onto a new account. This can allow you to get on top of your debt, but, you’ll generally be charged a fee to do so. |

| Cash advance fee | When you withdraw money from an ATM with your credit card or buy foreign currency – this is referred to as a cash advance. When you perform either of these actions you will generally be charged a cash advance fee. |

| Late payment fee | Your credit card limit typically refreshes each month. At the end of your monthly period, you’ll receive your bill for how much you’ve spent. With credit cards, you don’t have to repay the full amount, but you’ll pay at least the minimum amount by the due date to avoid late payment fees. If you don’t, then you’ll likely be charged a late payment fee. |

| International transaction fee | If you use your card overseas or make a purchase online with an international merchant, you will likely be charged a fee. An international transaction fee can also be called a foreign transaction fee or a currency conversion fee. |

How to reduce credit card fees

Now that you’re armed with all of the information you need on types of credit cards and common fees, let’s get stuck into how to reduce credit card fees. Here are five things you could do.

1. Pay your card off in full before the due date

Each month, you will receive your credit card bill. If you don’t pay this off by the due date, you will be charged late fees and interest. If you pay the full amount off each month, not only will you avoid late fees, but you’ll also avoid having to pay interest on the amount carried over into the next month. This is a great way to reduce credit card fees.

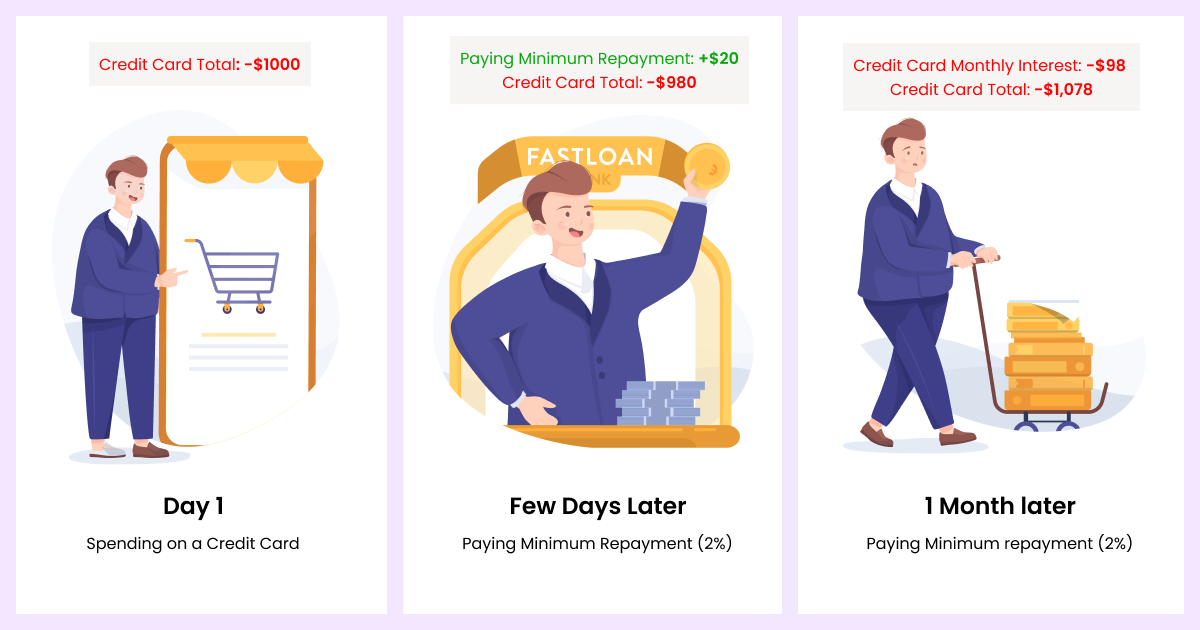

Or, at least make your minimum repayment by the due date

If you can’t repay your credit card balance off in full each month, you should try and at least make your minimum repayment. Your minimum repayment is the lowest monthly repayment you can make without incurring late fees. The minimum monthly repayment is usually about 2 or 3% of the total amount you owe for the month.

By paying the minimum repayment by the due date, you won’t have to pay late fees. However, you’ll still accrue interest on what’s still owing, and this could cost you a lot in the long run.

Therefore, if you want to reduce credit cards fees, you could try and repay your balance off in full each month, or at the very least, make your minimum repayments. It is also worth highlighting that many credit cards, especially low-interest rate credit cards, will void the credit card offer or rewards system if you are late with a payment.

2. Opt for a low annual fee credit card

There are certain credit cards on the market that offer good deals for the annual fee. Some cards might offer a low annual fee and some might offer no annual fees either for a certain time or for the life of the card.

Whilst this is a good way to reduce credit card fees, it is important to highlight that many of these cards will offset the lower annual fee with higher interest rates. This could cost you more in the long run. That’s why it’s a good idea to weigh your options and see what’s the best decision for you.

3. Avoid using your credit card to make ATM withdrawals

When you use your credit card to withdraw money from an ATM, this is called a cash advance. Just like any other purchase you make with your credit card, you will need to pay this back. What’s more – most credit card providers charge a fee for cash advances. How much the fee is, depends on your specific card.

If you want to reduce credit card fees, you could do this by not using your credit card to withdraw money from an ATM. If you need to withdraw money from an ATM, you could use your debit card instead, which might not charge you any fees.

4. Don’t use your credit card for international transactions

If you want to avoid being charged a fee for international transactions, there are two ways you can go about this. The first is you can shop around and look for a credit card that doesn’t charge a fee for international transactions. Alternatively, you could avoid making foreign transactions on your card altogether. Either of these options could help you reduce credit card fees.

5. Do your research before applying for a credit card

The final tip to reduce credit card fees is to do your research before applying for a credit card. Think of why you want a credit card and then try and find the best one for your needs. You could compare interest rates, fees, and find one that best aligns with your needs.