If you understand your credit score, then you can utilise your credit rating to its full potential. However, it can be hard to find how credit scores in Australia work. That’s because an internet search can often produce results based on credit scores in the United States. Although there are many similarities between credit scores in Australia and the US, there are some key differences. Today, we’ll take you through what those are.

Credit bureaus in Australia vs the US

In Australia, the three credit bureaus are Equifax, Experian and illion. America also has three major credit bureaus – two of which you might recognise – Equifax, Experian and TransUnion.

We’ve already covered Equifax and Experian quite a lot here at Tippla, so we’ll introduce you to TransUnion. Operational in more than 30 countries, TransUnion is an American consumer credit reporting agency. The company collects and aggregates information for more than one billion individuals across the world.

In the US, credit bureaus perform a similar role to Australia. Specifically, the bureaus collect credit information, generate credit scores and reports, to allow credit providers to properly assess the risk associated with potential borrowers.

Credit Scores in Australia

In Australia, you have three credit scores, one each from Equifax, Experian and illion. Credit scores in Australia are calculated by each of the bureaus using their own algorithms. Your credit scores are based on the information on your credit report.

This information includes:

Credit accounts;

Credit enquiries;

Repayment history;

Defaults;

Negative entries.

Your credit score is one of the multiple factors used by credit providers to decide whether they will accept your application when you apply for credit (a loan, credit card, utilities, post-paid phone plan and more). They might also check your bank statements, employment status and eligibility, among other criteria.

Credit scores in the US

Although your credit score is important here in Australia, in the United States, it can carry a lot more weight. Furthermore, the credit bureaus across the pond have a system that they commonly use to calculate credit scores – Fair Isaac Corporation (FICO).

Whilst America also uses Comprehensive Credit Reporting (CCR), they do calculate credit scores differently, and some of the information they include on credit reports is different from how we do it in Australia.

Here are some of the things that go onto your credit report and make up your FICO score:

Payment history

Amount owed

Length of credit history

New credit

Credit mix

Just like in Australia, the three CRAs in the US collect information differently. Therefore, American residents can have three different FICO scores, depending on which bureau they check with.

What are the differences between Australia and the US?

You already know a few differences already between credit scores in Australia and the US. But let’s look into the main differences a little deeper.

Credit utilisation

The credit utilisation rate (or ratio) is the amount of credit you have currently used divided by the total amount of revolving credit you have used. As an example, say you have a credit card with a limit of $10,0000, but you only spend $3,0000 every month, then your credit utilisation ratio is 30%.

In America, your credit utilisation rate carries a lot of weight when it comes to your credit score. However, in Australia, your credit utilisation ratio does not factor into the calculations of your credit score.

Credits score calculations

As we already highlighted, in the US, they mainly use the FICO system to calculate credit scores. In Australia, the bureaus do not use this system to calculate your credit scores.

Different scales are used

For credit scores in Australia, Equifax uses a scale ranging from 0 – 1,200 to rank credit scores. Experian and illion use a scale spanning from 0 – 1,000. The FICO system, however, uses a range of 300 to 850. On this scale, anything above 720 is deemed to be an excellent credit score.

Credit scores in Australia vs the US

Whilst there are some similarities between credit scores in Australia and in the United States – there are some key differences in the way credit scores are used and calculated. Because of this, when doing your own research on credit scores – be sure to check that you are looking at Australian resources. This way you know you’re getting the right information for you.

Does my Australian credit score count overseas?

Unfortunately, there isn’t an international credit score. Therefore, your Australian credit score won’t count if you move overseas. This means if you move overseas, you will need to build your credit history from scratch.

Credit scores don’t work the same across the world. Australia, the United Kingdom, Canada and the United States have similar credit scoring systems – but there are key differences between them. That’s why it’s a good idea to research what the credit scoring system is in whatever country you live in, to ensure you’re protecting your credit score.

We have covered what can affect your credit score frequently here at Tippla. But one question we get asked a lot is “how often does my credit score change?” You asked, so we have answered!

Who calculates your credit score?

Your credit score is a number ranging from 0 – 1,200. In Australia, your credit scores are calculated by three companies – Equifax, Experian and illion. These three companies are known as credit bureaus or Credit Reporting Agencies (CRAs).

Equifax, Experian and illion collect your credit information from credit providers across Australia. Credit providers can be banks, non-bank lenders, credit unions, utility companies and more.

The credit bureaus in Australia collect your credit information and use it to create your credit report. Your credit report is a document outlining your recent credit history. The information on your credit report is used by each of the CRAs to calculate your credit score.

Because there are three credit bureaus in Australia, you have three separate credit scores and reports – one with each credit bureau. Your credit scores and credit reports can vary among the credit bureaus. For a full breakdown of why that’s the case, take a look at our guide outlining why your credit scores are different.

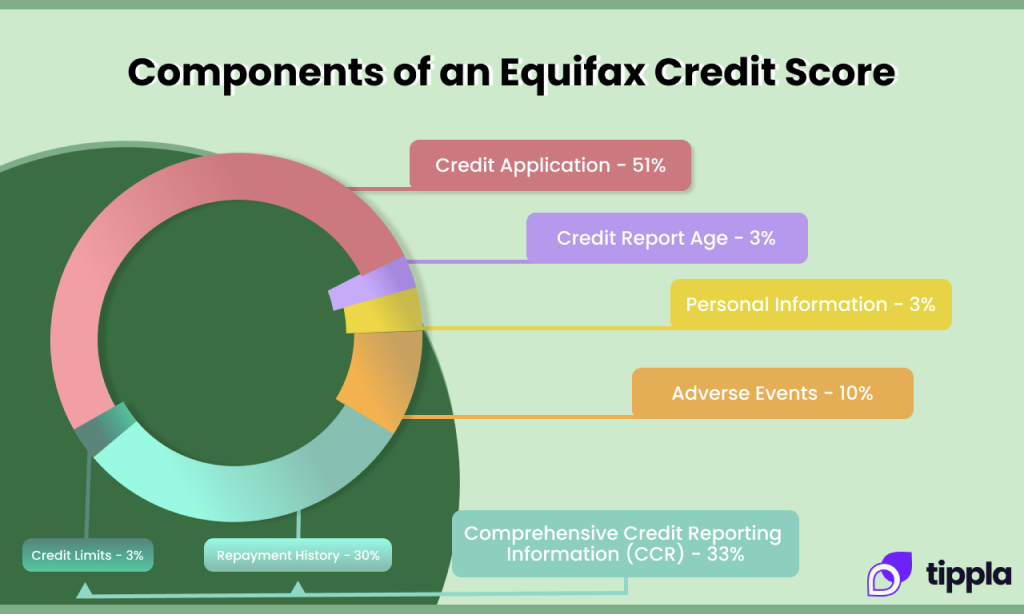

Equifax have provided the following information on how they calculate their Credit Score.

“The Equifax Credit Score is a numerical expression of your risk profile and ability to repay a debt. The higher the score the lower the risk. Our unique algorithm looks at the relative rating of your credit behavior against the ratings of the entire Australian population – with scores generated on request and at a point in time, to ensure the most comprehensive and accurate assessment”.

What information goes onto your credit report?

Your credit score is calculated using the information on your credit report. But what exactly is this information? To put it simply, it’s your recent credit history. When you take out a loan, credit card, utilities, post-paid phone plan and more, this is a type of credit. The way you manage that credit is what goes onto your credit report.

Specifically, here’s what information goes onto your credit report:

Credit accounts – if you currently have a loan, an active credit account, or a post-paid phone plan, then this is referred to as a credit account. Your credit report will list all of your open (current) credit accounts, as well as any accounts you have closed in the last two years;

Credit enquiries – whenever you apply for credit, this is called a credit enquiry. Credit enquiries will appear on your credit report for up to five years;

Repayment history – each time you make your fortnightly or monthly repayment for your loan, credit card, phone plan, or utilities, this is your repayment history. Your repayment history over the last two years will appear on your credit report.

Defaults – just like your repayment history appears on your credit report, so do your defaults. If you default on a repayment, then this will feature on your credit report for up to five years.

Negative entries – Negative entries can include court judgements, bankruptcies and serious credit infringements. Depending on the information, it can appear on your report for typically five to seven years.

Personal Information- Name, address, date of birth and employment.

Credit Report Age – How long you have held a credit history.

How do credit bureaus get my credit information?

So how exactly do the credit bureaus get your credit information? They get it from the source. If you have a credit card with a bank, then each month, that bank will send your updated credit information to the credit bureaus. This goes for all credit providers.

That information can be anything that we outlined above – your repayment history, whether the account is open or you closed the account within the month and more.

When exactly credit providers send the information will depend on the company. Some might create their reports at the beginning of the month, some could send it towards the end. The timing will depend on their own reporting procedures.

It’s important to highlight here that credit providers don’t necessarily send your credit information to all three of the credit bureaus. Whilst some banks and credit providers will report your credit information to Equifax, Experian and illion, some might only report to one or two of the credit bureaus. That’s one of the reasons why your credit score can vary among the CRAs.

How often do credit bureaus update my credit report?

Because the credit bureaus receive new credit information each month, your credit report is updated around once a month. Each time your credit report is updated, the new information will be added to your credit file.

Furthermore, all of the information on your credit report expires after a certain time. Sometimes when your credit report is updated, some information may be removed from your credit report because it has expired.

How often does my credit score change?

Your credit score is based on your credit report. Therefore, because your credit report is updated on a monthly basis, then your credit score can change each month. Whether your credit score changes will depend on what new information the bureau receives.

If any negative information has been reported to the bureaus over the past month, then your credit score might have dropped. Or, if positive information is reported, or previous negative entries expire on your credit file, then your credit rating could have received a boost.

How often does my credit score change on Tippla?

On Tippla, we get your credit report and credit score information directly from Equifax and Experian every 90 days. We refresh your credit reports every three months, based on the information provided to us by the two credit bureaus.

Therefore, if you take out a new type of credit, such as a credit card, or a negative entry is set to expire, this may not appear on your credit report straight away. The information will be updated whenever the latest 90 day period has ended.

What if there’s a mistake on my credit report?

Sometimes, new information will be added to your credit report but it won’t be correct. This can happen for a number of reasons, but it’s actually quite common. 1 in 5 credit reports have some kind of mistake on them.

So what can you do if there’s a mistake on your credit report? Firstly, don’t panic. You can get mistakes removed from your credit file. There are two steps you can take to have a mistake removed from your credit report.

Reach out to your credit provider – if the mistake involves a credit provider, such as an incorrect default, a credit enquiry you never made, or an issue with your credit accounts, then you can reach out directly to the company involved. If they agree that a mistake has been made, then they will alert the credit bureaus of the mistake and your credit report will be updated.

You can also reach out to the credit bureaus directly and ask them to handle the issue.

If you want to reach out to Equifax, you can request a correction to your credit report here. If it’s Experian you want to handle the mistake, then you can send them an email at this address creditreport@au.experian.com.

Your credit score can have far-reaching implications for numerous aspects of your life. It can be the difference between you being accepted or rejected for credit. That’s why it’s important to know how credit scores in Australia work. That’s why we’ve put together this handy overview of how credit scores work.

Who calculates your credit scores in Australia?

In Australia, you have three credit scores and credit reports. Why’s this? Because there are three credit bureaus, also known as Credit Reporting Agencies (CRAs) in Australia. The three credit bureaus in Australia are Equifax, Experian and illion. Your Equifax credit score will range between 0 – 1,200, whereas your Experian and illion will fall somewhere between 0 – 1,000.

A credit bureau is a company that collects information associated with the credit scores of individuals. This means if you have any type of credit (a loan, credit card, utilities, etc) then the company you have this credit with (bank, non-bank lender, utility company, etc) will report the information associated with the credit to the credit bureaus. This can be your repayment history, credit limit and more.

The CRAs then collect this information and use it to generate your credit reports and calculate your credit scores. They then make your reports and scores available to credit providers (following your consent) to help them make informed decisions. You have one credit score and one credit report with each of the three bureaus.

How do the CRAs calculate your credit score?

Equifax, Experian and illion each individually calculate your credit scores. They calculate your credit scores based on the information contained on your credit report. This includes:

Your active credit accounts, as well as any accounts closed in the last two years;

Your repayment history from the past two years;

Credit enquiries – every time you apply for a loan or other form of credit, it will appear on your credit report and remain there for five years;

If you have defaulted on a credit repayment, it will appear on your credit report;

Negative entries such as bankruptcy, court judgements and serious credit infringements will appear on your credit report.

The exact formula each of the credit bureaus use to calculate your credit score remains a well-kept secret, however, Equifax has provided the below overview of how it typically calculates credit scores in Australia.

Source: Equifax

What harms your credit score?

Following the introduction of Comprehensive Credit Reporting (CCR), a combination of positive and negative information goes onto your credit report and is used to calculate your credit report.

Some good habits, such as consistently meeting your credit repayments, having a good mix of credit accounts (but not having too many), and not too many credit enquiries on your report can all contribute positively to your credit score.

However, there are also some things that can harm your credit score. We’ve listed some of the items that can harm your credit score below:

Credit enquiries – when you apply for credit and the company you apply with checks your credit report, this is known as a hard enquiry. Hard enquiries harm your credit score, and the more applications you make in a short period of time, the worse the damage.

Defaults – if you default on one of your credit repayments, then this will appear on your credit report and lower your credit score. Defaults will remain on your credit report for up to five years.

Too many credit accounts – if you have too many credit accounts, such as multiple loans and credit cards, then this could indicate that you’re in financial stress. Therefore, when calculating your credit score, too many accounts can lower your score.

Negative entries such as bankruptcy, court judgements and serious credit infringements can also harm your credit score as they suggest that you have not been able to handle your debt effectively in the past.

If your credit score isn’t where you want it to be, check out Tippla’s guide on how to improve your credit score.

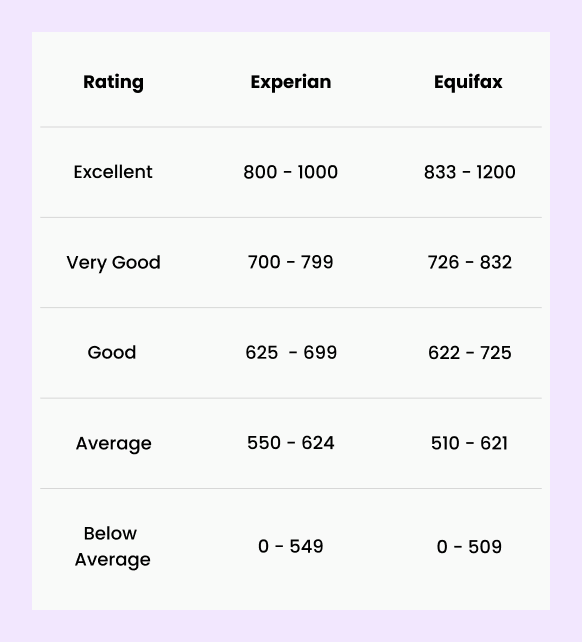

What is a good credit score?

A good credit score in Australia varies among the bureaus. Specifically, your credit score will fall somewhere on a five-point scale. This scale ranges from below average, average, good, very good and excelled.

Here’s how Equifax and Experian rank your credit scores:

Source: Equifax and Experian

A good credit score for illion ranges from 500 – 699, whereas a great credit score falls between 700 – 799 and an excellent score sits from 800 – 1,000.

What are credit scores used for?

Your credit score is used to assess your creditworthiness (translation: how reliable of a borrower you are). Your credit score provides an overview of how well you have managed your credit debt in the past and therefore indicates how likely you will be to repay any further debt you take on.

What does this mean in basic terms? When you apply for a loan (such as personal loans or home loans), credit card, or any other form of credit, the company you are applying with want to know how likely you are to make your repayments.

A good credit score (or higher) indicates that you will likely make your repayments and you’re therefore a lower risk. An average or below-average credit score can imply that you might struggle to make your repayments, and could be at risk of defaulting.

With this in mind, your credit score is one of the factors credit providers use to assess how big of a risk you are and helps them determine whether they will accept your reject your credit application.

Who can view your credit score?

The purpose of your credit scores in Australia is to help credit providers determine how risky of a borrower you are. Therefore, the only companies that can view your credit score are the ones you have applied for credit with.

When you apply for credit, typically in the terms and conditions, you will consent to having your credit score and report checked by the company. Some credit providers will only look at one credit score and report, however, others might look at two or all three. That’s why all of your credit scores matter, and no one score matters more than the others.

In Australia, you have three credit scores – one each from the three credit reporting agencies (CRAs), also referred to as credit bureaus – Equifax, Experian and illion. Today, we’re going to explore which credit score matters most out of the three.

What is a credit score?

Let’s cover some basics first – what is a credit score? A credit score is a number that falls somewhere on a scale between 0 and 1,200. This number represents your creditworthiness, which basically means, how reliable of a borrower you are. The higher your credit score, the more reliable you are perceived to be.

Your credit score is calculated by the information contained in your credit report. Banks, non-bank lenders, credit unions and other credit providers are required to report their credit information to the CRAs in Australia. The information they report includes credit enquiries, credit accounts, defaults, repayment history and more.

Your Equifax credit score

Equifax is the largest of the three credit bureaus in Australia, with a presence around the world. Your Equifax credit score is based on the information reported to Equifax by credit providers and calculated using the company’s credit scoring algorithm.

Whilst we don’t know the exact algorithm used by Equifax, the company has outlined the general factors considered in credit score calculations as follows:

The number of accounts you have;

The types of accounts;

The length of your credit history;

Your payment history.

Furthermore, the CRA has provided the following information on how they typically calculate your credit score:

Source: Equifax

Your Experian credit score

Experian is another credit bureau in Australia that calculates your credit score and report. Whilst the company is similar to Equifax, it is known for being the more data-driven out of the three credit bureaus in Australia.

As highlighted by the bureau itself: “Your Experian Credit Score is calculated applying a statistical algorithm that uses past events to predict future behaviour. Each credit bureau uses a slightly different algorithm and does not disclose in detail how this is calculated.”

Nonetheless, Experian outlines the following key attributes that are used to generate your credit score. This includes:

Type of credit providers that have made enquiries on your report;

The type of credit you have applied for;

Your repayment history;

The credit limit of each other credit products;

Negative entries;

The number of credit enquiries (credit applications) you have made.

Your illion credit score

illion outlines on its website that it determines the credit ratings of individuals by looking at whether you are reliable with paying your bills.

Specifically, the credit bureau states that the following events could harm your credit score:

Not paying your bills on time, or failing to pay them at all;

Applying for credit too often;

If someone else defaults on a joint debt.

Why is my credit score important?

Let’s now take a look at why your credit score is important. A lot of people might have heard about their credit score, some people might even know what their credit score is, but a lot of people might not know why their credit score matters.

Your credit score and accompanying credit report is one of the key ingredients that lenders and credit providers use to determine whether to accept or reject your credit application. Whilst your credit score isn’t the only factor they consider, it is an important piece of the puzzle.

Because of this, your credit score and report can be the difference between you being accepted and rejected for credit. That’s one of the main reasons why your credit score is important.

Which credit score matters most?

Out of your three credit scores, which one matters the most? Unfortunately, it’s not such a clear-cut answer. When you apply for a loan, credit card, or another type of credit, the company you are applying to will check your credit score and credit report.

It will depend on the company as to which credit report they will check. Some companies might only check one of your credit reports and scores, however, others might check two, or even all three.

Therefore, when it comes to which credit score matters most, the simple answer is – all of them. Any of your three credit scores can be used to assess your creditworthiness. That’s why it’s important to ensure that all the information on each of your credit reports is accurate and up-to-date.

How to improve your credit score

If you have taken a look at your credit score, and you want to know how to improve it, here are a few ways you can improve your credit score.

Space out your credit applications

Did you know every time you apply for credit, it registers as a hard enquiry on your credit report? Hard enquiries harm your credit score, and they remain on your credit report for up to 5 years. This means, whenever you apply for new credit, the company you’re applying with can see your previous applications over the past 5 years.

With this in mind, if you want to limit the damage to your credit score, then you can space out your credit applications.

Don’t take on too much credit

If you have too many open credit accounts, such as multiple loans or credit cards, then it can negatively affect your credit score. Having too many credit accounts at once can make it appear like you are in financial distress, or have difficulty managing your finances. Therefore, you are perceived to be a more risky borrower.

One way to avoid this preconception is to only take out credit when you need it. This way, you could avoid having too many credit accounts open at once.

Make your repayments on time

Your repayment history is one of the factors the credit bureaus consider when calculating your credit score. Therefore, in order to improve your credit score, or maintain a good credit score, you could make sure that you make your repayments on time.

If you can demonstrate that you can effectively manage your debt by consistently meeting your repayments, this can go a long way to proving your creditworthiness.

Have you noticed a drop in your credit score? You might be wondering why it has fallen – Tippla has put together a number of reasons why that might be.

Your credit score is an important number and can have far-reaching implications. Today, Tippla is going to answer the question “why has my credit score fallen”, but first, let’s go over some important information.

What is a credit score?

A credit score is a number ranging from 0 – 1,200. This number is a representation of your creditworthiness (translation: how reliable of a borrower you are). In Australia, your credit score is calculated by three credit bureaus – Equifax, Experian and illion. Therefore, you have three unique credit scores and credit reports.

Why is my credit score important?

You might be wondering why is your credit score important. Putting it simply, when you apply for some kind of credit, such as a loan, credit card, utilities and more, your credit score is one of the factors that lenders look at when deciding whether to approve or reject your application.

Whilst it isn’t the only factor that lenders consider – it is an important factor. Having a good credit score could be the difference between you being approved or rejected.

Not only that, but your credit score can influence the finance available to you. If you have a bad credit score, then you will likely be deemed as a higher risk. Because of this, credit providers will typically only offer you products with higher interest rates, lower borrowing limits, and stricter conditions in a way to offset the risk they perceive you to be. Therefore, you will likely have limited choices that can be more costly than if you had a good credit score.

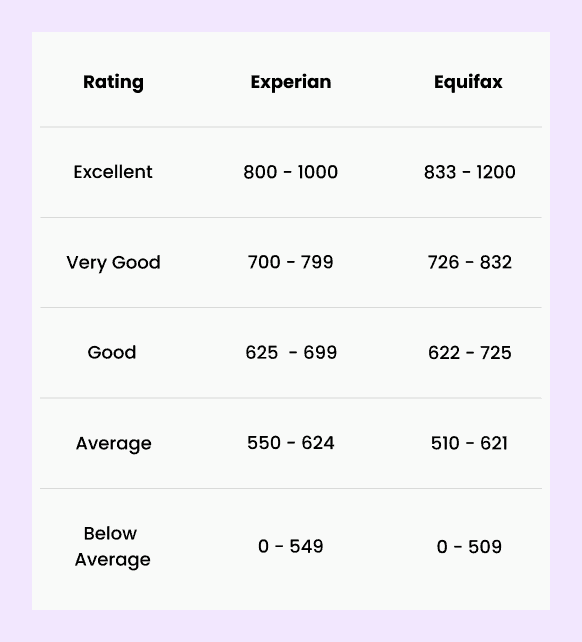

Not sure what is a good credit score? Equifax and Experian calculate your credit scores differently. Here’s how they categorise credit scores:

Source: Equifax and Experian

How is a credit score calculated?

Let’s take a quick look at how credit scores are calculated. Whilst the exact formula of how credit scores are calculated remains a well-guarded secret, and each of the bureaus uses different algorithms to calculate your scores, we do know a few things.

The credit bureaus use this information on your credit report to calculate your credit score. Equifax has given us the below information into how they typically calculate a credit score:

How Experian calculates your credit score

Experian, on the other hand, has outlined the following: “Your Experian Credit Score is calculated by applying a statistical algorithm that uses past events to predict future behaviour. Each credit bureau uses a slightly different algorithm and does not disclose in detail how this is calculated.”

However, the credit agency has outlined the following as key attributes it uses to generate your credit score:

Type of credit providers that have made enquiries on your report

The type of credit you have applied for

Your repayment history

The credit limit of each other credit products

Negative entries

The number of credit enquiries (credit applications) you have made

Why has my credit score fallen?

Now you know what information goes onto your credit report, and therefore, what can influence your credit score, let’s now tackle the question “why has my credit score fallen?”.

Unfortunately, there is no single reason as to why your credit score could have fallen. The exact reason will depend on your personal circumstances. However, there are a number of things that can harm your credit score. Let’s look at these first.

A large number of credit applications in a short period of time

Open accounts with debt collection agencies

Short term credit

Missed payments

Bankruptcy actions

Defaults

Court judgements

Common reasons why your credit score could have fallen

So what are some of the common reasons why your credit score has fallen? We’ve put together a list below. Whilst this list gives a good overview, it is not exhaustive, and might not apply to your individual situation.

Making too many credit applications in quick succession – have you recently applied to multiple lenders for a loan, a credit card, or some other form of credit? Each time you apply for credit, it registers as a hard enquiry on your credit report and lowers your credit score.

Defaulting on a credit repayment – did you miss a repayment on your loan or credit card? This could appear on your credit report as a default and harm your credit score;

Having too many credit accounts open – if you have multiple loans, or multiple credit cards, as an example, open in your name then this could be harming your credit score. Having too many credit cards can indicate that you are in financial distress and therefore, are a risky borrower;

For a more in-depth guide on negative entries that can harm your credit report, check out one of our recent articles on negative entries on your credit report.

Can I improve my credit score?

Yes, you can improve your credit score! Whilst it won’t necessarily be an overnight fix, it can be done, and most of the fixes can be done yourself for no cost at all. If you’re thinking of paying a company to help you fix your credit report, then check out our article on whether credit repair companies are worth it.

Every time you apply for credit, with limited exceptions, the company you are applying with will check your credit report to get an overview of your credit history and determine if you are a risk. This is called a hard enquiry.

A hard enquiry harms your credit score. Therefore, in order to limit the damage to your credit score, the fewer applications you make, the better. That doesn’t mean that you shouldn’t ever apply for credit, but instead, do your research beforehand and find the best deals suited to your requirements, and check that you meet the eligibility criteria.

Don’t take on too much credit at once

Having multiple loans, credit cards or a mixture of multiple credit accounts can be damaging for your credit score. Why is this? Because it can appear like you are in financial distress. Therefore, one way you can avoid having too many credit accounts open at once is to only take on credit when you really need it, or there is a clear purpose for the credit.

Make your repayments on time

As we highlighted earlier, repayments decently contribute to your credit score. Therefore, in order to improve your credit score, or maintain a good credit score, you should ensure that you make your repayments on time.

Displaying that you can effectively manage your credit can go a long way in proving that you are a reliable borrower and therefore, have high creditworthiness.

Want to know what goes on your credit report, and how long that information remains on your credit file? Then Tippla has the perfect guide for you.

Your credit report is an important document and it can have far-reaching implications. Any time you apply for a loan, credit card, mortgage, utilities, even a phone plan – your credit report plays an important role. That’s why we’re going to answer the question “what goes on my credit report”, as well as delve into how long information remains on your file.

What is a credit report?

A credit report is a document that outlines your recent credit history. Your credit history is an account of your credit activity. As outlined by Experian, credit is the ability to borrow money or utilise goods or services, with the understanding that you will repay the credit at a later date.

So your credit history is an account of any time you have used credit – whether it be a loan, credit card, utilities, phone plan and more. Your recent credit history appears on your credit report.

In Australia, you have three credit reports from the three credit bureaus in Australia – Equifax, Experian and illion. The information listed on your credit report is what’s used to calculate your credit score. Your credit score is a number ranging from 0 – 1,200 and provides an indication of your creditworthiness.

Why does my credit report matter?

Whenever you apply for credit (with limited exceptions), the company you are applying for credit with, will check your credit report. They do this to see how risky of a borrower you are.

Lenders will check the information on your credit report to look out for any red flags – do you have defaults on your report? Have you recently made a lot of credit applications recently which might indicate that you’re in financial difficulty? Or do you have a stellar credit report and a good credit score? These are some of the things credit providers will look out for when making their decision.

Whilst your credit report and credit score aren’t the only factors companies will consider when deciding whether to lend to you, it is an important piece of the application process. That’s why it’s a good idea to employ good credit behaviour to maximise the likelihood of being approved for a loan.

What goes on my credit report?

There is a lot of information that goes onto your credit report, but we’re here to break it down for you. Below is an outline of the information that can be stored on your credit report, if it’s applicable.

Credit enquiries

When you apply for a loan, credit card, or even utilities, this is known as a credit application or credit enquiry. As part of your application, typically in the terms and conditions, you are giving the company you’re applying with permission to check your credit score and credit report. When they check your credit report, this is referred to as a hard enquiry.

Each time you apply for some type of credit, and the resulting hard enquiry is made, it will appear on your credit report. This will occur regardless of whether you are accepted or rejected for the credit you apply for.

There are two types of enquiries – a hard enquiry or a soft enquiry. The main difference is that a hard enquiry is made after you have applied for money, whereas a soft enquiry is unrelated to lending you money.

Specifically, a hard enquiry is when a lender checks your credit report following a credit application. Hard enquiries harm your credit score and remain on your credit report for up to five years.

Soft enquiries, however, do not harm your credit score. Soft enquiries are when someone runs a credit check on you, but it’s unrelated to money. This could be a pre-approved credit offer, or platforms like Tippla, that allow you access to your credit report for free.

Credit enquiries appear on your credit report because it gives lenders insight into your financial situation. If you have lots of enquiries on your credit report, it could symbolise that you are in financial difficulty and are likely to default on your repayments.

Few, or even no credit enquiries, could suggest that you are responsible with your finances. Whilst both of these scenarios might be false, or not paint the whole picture, this is what credit enquiries on your report may suggest.

According to Equifax, when it comes to credit enquiries, they will provide the following information on your credit report:

Type of credit provider;

The type and size of credit requested in the application;

The pattern of credit enquiries over time.

Credit accounts

Similar to credit enquiries, and credit accounts that you currently have open will appear on your credit file. Are you currently repaying a loan? Do you have an active credit card? Then this will appear on your credit report.

Repayment history

Your repayment history is an important part of your credit report. Your repayment history is information that outlined whether you have met your credit payment obligations in a given month. Basically, your repayment history shows whether you paid the amount owing on your loan, credit card, etc by the due date.

Defaults

Similar to repayment history, defaults will also appear on your credit report. A default is a missed payment. According to the Office of the Australian Information Commissioner (OAIC), a credit provider can list a default on your credit report if:

the payment has been overdue for at least 60 days;

the overdue payment is equal to or more than $150;

a notice has been sent to your last known address to let you know about the overdue payment and requesting payment;

a second notice was sent at least 30 days later to let you know that if you don’t make a payment the credit provider intends to disclose the information to a credit reporting body;

the credit provider must wait at least 14 days after issuing the second notice before listing the default.

Other negative entries

Your credit report can also contain other negative entries, if applicable. This can include bankruptcies, court writs or judgements.

Personal information

Not only does your credit report contain your credit history, but it also contains some of your personal information about your identity. This includes your name, address and date of birth. It won’t, however, include information such as your marital status or salary.

How long does information remain on my credit report?

Now you know what goes onto your credit report, let’s take a look into how long items stay on your credit report. As we highlighted at the beginning of this article, your credit report is an overview of your recent credit history.

It won’t contain all the credit information you’ve accrued over the past 10 years. Items do expire after a time. This is particularly beneficial if you have a poor credit history – you can work to improve it, and it won’t always be a black mark on your credit report.

Here’s typically how long items remain on your credit report:

Credit accounts – your credit report will outline all of your current credit accounts, as well as any that you have closed in the past 2 years;

Credit applications – any application you have made for some type of credit will remain on your report for 5 years regardless of whether you were approved or rejected;

Repayment history – your repayment history over the past 2 years;

Defaults – if you default on a repayment then it will appear on your report for up to 5 years;

Court judgements and bankruptcies – 5 years;

Serious credit infringements – these can stay on your credit report for up to 7 years.

Can I get information removed from my credit report?

If you notice a mistake on your credit report, then you can take steps to have it removed from your credit report. You can either reach out to the relevant credit provider, or you can reach out to the credit bureau themselves and ask them to handle the mistake.

However, if the information on your credit report is correct, regardless of whether the information is negative and harms your credit score, it can’t be removed. You will need to wait for the allotted time period for that information to expire from your credit report.

In Australia, your credit score is calculated by three credit bureaus. Out of these three, the two largest for individual credit reports is Equifax and Experian. To help you understand what these companies do and what’s the difference between them, we’ve put together a comparison of Equifax vs Experian.

What are credit bureaus?

A credit bureau, also referred to as a Credit Reporting Agency (CRA), is a company that collects information associated with the credit scores of individuals. If you have any type of credit – say a loan, credit card, or utilities, then the company you have that credit with will report that information (repayment history, credit limit, etc) to a credit bureau.

CRAs collect all the information reported to them and generate credit scores and credit reports for individuals. They then make that information available to banks, non-bank lenders, and other credit providers, with the individual’s consent to allow them to make informed decisions when extending credit.

What are the different types of credit?

Many things can be classified as credit, and the list could surprise you. It’s not just a credit card that you need to be careful with. Here is an overview of some of the types of credit:

Credit can include:

Loans – such as a personal loan, mortgage, business loan, short-term or payday loan and more;

Credit and store cards;

A mobile phone plan;

Internet services;

Utilities – water, electricity and gas;

Hire purchases.

How do credit bureaus receive their information?

Every time you apply for credit, whether it be a loan or utility account, the company that you apply with will send this information to one of the credit reporting agencies so it can be included on your credit report.

Your information will be reported even if you’re not approved for the loan. If you are approved for the loan, then this, along with your repayment history – especially if you default on a repayment, will also be reported on a monthly basis.

In addition to your credit information, public information such as whether you have entered into bankruptcy, or court listings, will be reported to the credit bureaus.

Which CRAs operate in Australia?

In Australia there are three CRAs – Equifax, Experian and illion. Equifax and Experian are the two largest credit bureaus for individual credit scores. This means you don’t have just one credit score and report, you actually have three credit scores and reports – one with each CRA.

Equifax – Equifax is the largest of the three credit bureaus in Australia. It provides both personal and business credit reports across the country. If you want your credit report directly from Equifax, you can order a free copy of your report and receive it in 10 days. However, you can only do this once every 12 months.

Experian – Just like Equifax, you can order a free copy of your credit report with Experian. A subtle difference between the two companies is that Experian is more data-focussed. The company allows credit providers to make more informed decisions through data sharing.

illion – illion, which was formerly known as Dun & Bradstreet, provides credit reports for both individuals and companies. The credit bureau also providers debt recovery services.

Equifax vs Experian: What’s the difference?

Let’s tackle the main question – Equifax vs Experian: What’s the difference? Whilst both of these companies perform a similar role, there are some differences.

Today, we’re only going to look at the differences that concern Australian residents in regards to their credit score. There are likely many differences on a business-level, in terms of company structure, company size, geographic footprint, profit and revenue, and more.

1. How Equifax vs Experian calculates your credit score

One of the main differences between Equifax and Experian is how they calculate your credit scores. Equifax measures your credit score on a scale ranging from 0 – 1,200, whereas Experian’s scale only goes from 0 – 1,000. Because of this, you might have different credit scores across the bureaus.

Your Equifax credit score

Not only is the range they use different between the two CRAs, but also, the algorithms they use to calculate your credit score are different. Whilst the exact formula they use is a well-kept secret, the general factors Equifax considers in its credit score calculations are as follows:

Type of credit providers that have made enquiries on your report;

The type of credit you have applied for;

Your repayment history;

The credit limit of each other credit products;

Negative entries;

The number of credit enquiries (credit applications) you have made.

2. Which companies report to Equifax or Experian

Another difference between the two bureaus is the companies that report to them. If you are a credit provider, you don’t have to report your customer’s credit information to both bureaus. Because of this, one lender might only report to one credit bureau, whilst one bank might only report to the other.

That means your credit scores can differ across the two bureaus. In fact, you could have a credit score with one bureau, but none with another, because of this reason.

Which credit bureau matters the most?

One question we get asked at Tippla quite often, is which credit bureau matters the most? Unfortunately, that’s not such a straightforward question, as they all matter. Whilst Equifax is the largest out of the three, you have a credit score and report with each of the bureaus and either one of these can be accessed by a credit provider when you apply for some form of credit.

Why does my credit score matter?

Equifax, Experian and illion are all responsible for calculating your credit score. But why does your credit score matter in the first place? Putting it simply, your credit score and credit report is one of the factors considered by credit providers when they are reviewing your application. They use your credit score to determine whether they will lend you money or extend you credit.

Because of this, your credit score could be the difference between you being accepted or rejected for credit. If you have a good credit score, then this will strengthen your application. If you have a below-average credit score, then this could hinder your application. In a worst-case scenario, it could even lead to you being rejected for credit.

Your credit score can influence the following:

Whether you are approved or rejected for credit;

Your interest rate;

Your borrowing limit;

Other credit conditions, such as fees and charges.

Whilst your credit score isn’t the only factor credit providers consider, it is an important element. Credit providers might also check the following:

Your bank statements;

Employment status and income;

Government benefits;

Gambling;

Eligibility for a loan – are you a citizen/resident and are you over 18 years of age.

How to improve your credit score

If you have a below-average credit score, then there are a number of ways you can improve your credit score. Tippla recently put together a helpful guide to steer you through the process, but to sum it up, here are a few things you could try:

If you’re in the market for a phone plan, there’s something you should be aware of. A phone plan is a type of credit. Therefore, the answer to the question “do phone plans affect your credit score?” is yes. Tippla has outlined how and why your phone plan influences your credit rating below.

What is a phone plan?

A phone plan (also referred to as a post-paid plan) is a contract where you get a phone, as well as voice, SMS and data inclusions for a single price. With a plan, you don’t have to pay for the phone outright, instead, you pay a monthly fee at the end of the month which includes the cost of the phone as well as your usage. If you take on a phone plan, you don’t own the phone until you’ve paid it off.

Postpaid vs prepaid: what’s the difference?

Postpaid and prepaid are the two main types of phone deals you can have in Australia. The main difference between postpaid and prepaid is when you pay for the service. As we mentioned above, with a postpaid phone plan, you pay at the end of the month and pay based on your usage.

With a prepaid plan, however, you pay at the beginning of each month. Typically with a prepaid plan, you pay a fixed monthly amount for pre-determined parameters, such as your monthly data, text and phone calls.

In addition, with a prepaid plan, you generally need to already own the phone you use. Whereas with a postpaid plan, the phone often comes with the plan and can be used as a way of buying the phone you want without having to pay the full amount upfront.

Why would you get a postpaid phone plan?

There are a number of reasons why you might want to get a postpaid phone plan. The main reason would be if you want to buy a new phone, but you don’t want to pay for it outright. Taking on a phone plan can allow you to purchase a new phone and pay it off in instalments, as well as cover your phone and data usage.

With a prepaid plan, you pay a fixed amount each month and as a result, you get a set amount of inclusions: data, texts and calls. If you exceed your set inclusions, then you will need to recharge your phone again.

With a postpaid plan, however, because you’re not paying your bill until the end of the month, you can exceed your plan’s limitations. Whilst you will have to pay for the extra usage, you don’t have to worry about not being able to use your phone if you do go over.

Who offer phone plans in Australia?

In Australia there are three mobile networks – Telstra, Optus and Vodafone, also referred to as telecommunication companies (or telcos). Whilst these three networks do offer wide coverage, the quality of the coverage will depend on where you live and what mobile communications standard your phone can connect to (3G, 4G or 5G). This is especially true for regional and rural areas.

In terms of who offers phone plans, there are many telcos in Australia that offer phone plans. Telstra, Optus and Vodafone all offer their own phone plans based on their networks and these guys are the big three telcos in Australia. However, there are many smaller telcos that offer a range of plans, but they’re all based on one of the three networks.

In fact, in Australia, you can get a phone plan from your supermarket, with Coles, Woolworths and Aldi all offering their own phone plans. But there are a range of other providers such as dodo, iinet, Moose, TeleChoice – the list goes on and on.

That’s why it’s a good idea to know what network will offer you the best coverage based on your location and needs. Once you’ve determined this, you can shop around for a phone plan that meets your usage needs, such as the amount of data you want, texts and phone call limits.

There are a number of comparison sites that have compiled many of the phone plans on offer. However, they don’t necessarily show all of the options out there. That’s why it’s good to shop around online.

How do phone plans affect your credit score?

Now let’s tackle the next question – how do phone plans affect your credit score? Just like a loan or credit card, a postpaid phone plan is considered to be a line of credit. A prepaid phone plan is not a line of credit as you’re paying for the service upfront.

1. Telcos will typically check your credit score

What does this mean? When you apply for a postpaid phone plan, the telco company you apply with will typically check your credit score, to see how reliable of a borrower you are. This check is known as a hard enquiry, and it will harm your credit score initially.

Regardless of whether you are approved for the phone plan, the hard enquiry will remain on your credit report for five years, as a credit enquiry (credit application). This means, for the next five years, any time you apply for a loan or some kind of credit, the companies you apply with will be able to see this credit enquiry on your report.

2. If you miss your repayments, it could harm your credit score

Going forward, if your application for the phone plan is accepted, then this will be listed as an active credit account on your report. If you default on your phone plan repayments, then this will also appear on your credit report. Initially, this will also harm your credit score. Furthermore, the default will remain on your credit report for up to five years, and any time you apply for credit, the company you’re applying with will see the default.

3. It can help you build a good credit history

On the reverse, a phone plan can help you build a good credit history and boost your credit score. If you can make all of your repayments on time, then this can go a long way to show that you are responsible with your finances.

The trick here is to remain on top of your repayments. Therefore, it’s a good idea to make sure you can comfortably afford your phone plan repayments before you apply.

Can you prevent your phone plan from impacting your credit score?

The short answer to this is yes, there are a number of things you can do to stop a phone plan from impacting your credit score.

1. Opt for a prepaid phone plan

Instead of getting a postpaid phone plan, you can instead get a prepaid plan. Nowadays, prepaid plans can offer really good deals, such as unlimited text and calls and large data limits.

If you take a prepaid phone plan, the company you buy it from won’t perform a credit check and because you pay for the service in advance, if you miss a payment, it won’t harm your credit score.

However, if you take out a prepaid phone plan, then you will need to pay for your phone outright or use the existing phone you’ve already paid for. So whilst a prepaid phone plan won’t impact your credit score, it isn’t always a suitable option.

2. Always make your repayments on time

As we highlighted above, if you take on a postpaid phone plan, if you default on a monthly repayment, then this will appear on your credit report. Not only will it harm your credit score, but it will also serve as a black mark on your report for up to five years.

In order to avoid this, it’s important to make your repayments on time. If you consistently make your repayments, then this can actually be good for your credit score and show that you are a reliable borrower.

3. Try not to exceed your plan limitations

In line with making your repayments on time, one way you can help yourself out with this is by making sure you don’t exceed the plan’s limitations. If you go over your data usage then your provider might give you extra data as a top-up automatically and charge you for the extra data – even if you don’t use it all. This is sometimes called an add on.

When you get close to having used all of your data, you will likely receive a text or an email from your provider, however, these can be easy to miss. Whilst one top-up might not cost much, if you end up needing several top-ups, it can get costly.

That’s why it’s a good idea to keep an eye on your usage as you go through the month and try not to exceed your limitations. You can also speak with your provider on whether you can disable automatic top-ups.

In Australia, you have three credit scores and credit reports. The information contained on your credit report can be the difference between you being approved or rejected for a loan. But who looks at your credit report and why? Tippla has the answers for you below.

What is a credit report?

A credit report is a document that contains your recent personal and credit financial information. What does this mean? If you have taken out any form of credit (a loan, credit card, utilities, phone plan, etc), then this will appear on your credit report.

Specifically, here’s a rundown of what information will appear on your credit report:

Personal information – such as your name, address, date of birth and employment;

Credit account information – all of the credit accounts you currently have open or have closed in the past two years, such as any loans, credit cards, utilities, and more;

Repayment history – your repayment history for your credit accounts will be listed on your report;

Credit applications – every time you apply for some kind of credit, regardless of whether you were approved or rejected, it will appear on your report;

Negative entries – this includes bankruptcies, defaults, public records and court judgements.

How long do items stay on your report?

Your whole credit history won’t appear on your report. All of the information has an expiry date. Here’s a rundown of how long you can expect information to stay on your report:

Credit accounts – all current accounts, and any that you have closed in the past 2 years;

Credit applications – 5 years;

Repayment history – your report will show your repayment history over the past 2 years;

Defaults – these will appear on your credit report for up to 5 years;

Court judgements and bankruptcies – 5 years;

Serious credit infringements – up to 5 years.

Why does your credit report matter?

When you apply for any kind of credit, whether it be a mortgage, or even a personal loan or electricity provider, they will check your credit report to see how risky of a borrower you are.

They will look at your credit score, a number ranging from 0 – 1,200 which is based on all of the information contained in your report, as well as your credit file. They will look at this information, as well as other documents that give them an idea of your financial situation, such as your bank statements, employment details, etc.

So, why does your credit report matter? It is one of the ingredients lenders, banks and other credit providers use to determine whether they will accept or reject your application. Therefore, your credit report could be the difference between you being accepted and rejected for a loan.

Who looks at your credit report and why?

With this in mind, who looks at your credit report, and why? Not just anyone can look at your credit report. Your friends, your neighbour, even your employer – none of them can access your credit report. Only companies that you permit to view your report can see your file.

Every time you apply for credit, you are giving the company you’re applying to permission to view your credit report. This permission will often be granted in the terms and conditions of the application. They check your credit report to get an idea of your creditworthiness and assess how much of a risk you are.

Therefore, any company that you apply for a credit card, loan, utilities, phone plan, and more with, can view your credit report – but, only if you permit them. However, generally speaking, if you don’t consent to a credit search, it’s unlikely your application will be processed.

There are a few loans out there that claim to not check your credit score. These are called “no credit check loans”. However, they are usually only small personal loans, and they often come with high interest rates and fees.

What do lenders look for on your credit report?

When lenders, banks, and other credit providers check your credit report, what are they looking for? Generally speaking, when a company looks at your file, they’re trying to get a sense of how reliable you are.

They will be looking out for any credit defaults, which indicates that you haven’t been able to meet your repayments in the past. They will also check how many open accounts you already have – too many can make you more of a risky borrower.

Other things they will look out for – negative entries, repayment history, maturity of your accounts, and more. The purpose of them checking your report is to get insight into whether you are likely to repay the amount you want to borrow.

Do you have a below-average credit score and want to improve it? Check out Tippla’s helpful guide on how to improve your credit score here.

Whilst your credit score is only a number, it actually can impact your life in a very real way. So why is your credit score important? Tippla has the answers for you below.

What is a credit score?

Before we answer the question “why is your credit score important” it’s important to cover the basics first. What is a credit score? If you’re not sure what a credit score is – you’re not alone. In Australia, 73% of Australians don’t know their credit scores or why they are important.

Your credit score is a number ranging from 0 – 1,200. This number represents your creditworthiness (translation: how reliable of a borrower you are). The higher your credit score, the more reliable of a borrower you are perceived to be.

What is a reliable borrower?

A reliable borrower is someone who makes repayments on time. If a person takes out a loan, a reliable borrower would be expected to make their monthly repayments on time and during the length of the loan, completely repay their debt plus interest.

For a lender, a reliable borrower is seen as less of a risk, as they are more likely to repay the loan in full. A risky borrower, however, might miss payments, or default on their repayments. This means the lender could lose money if the borrower can’t repay the loan. A risky borrower would likely have a below-average credit score.

Who can see my credit score?

Your credit score is sensitive information. This means, not just anyone can see your credit score. You need to provide consent in order for a company to see your credit score.

So when does this happen? Every time you apply for credit – this could be a loan, credit card, phone plan or utilities, you are giving the company you are applying to permission to view your credit score and credit report.

When the credit provider looks at your credit score and report, they can judge how risky of a borrower you are, and determine what products they would be willing to offer you. If you have a below-average credit score, your application could be rejected.

How many credit scores do I have?

In Australia, there are three credit reporting agencies (CRAs) – Equifax, Experian and illion. Equifax and Experian are the two largest global CRAs. Each month credit providers report consumer credit information to either of these three agencies. The information these agencies receive from credit providers is what they use to calculate your scores.

Because of this, you have not one, but three credit scores in Australia. You have one each from Equifax, Experian and illion, and an adjoining credit report which holds all the information your credit score is based on.

What’s the difference between your credit score and credit report?

Your credit report holds all of your recent credit history. This includes any current credit accounts – loans, credit cards, utilities, phone plan, etc. It will also have your repayment history for the last two years, any closed credit accounts from the past two years, and any negative entries (defaults, bankruptcy, court judgements, etc).

Your credit score is a number ranging from 0 – 1,200. Your credit score is based on the information held on your credit report. If your credit report shows a good credit history, then you will likely have a high credit score. However, if there are multiple negative entries on your credit report, then your credit score will likely be lower.

How are credit scores calculated?

This question is a bit tricky because the exact algorithm credit agencies use to calculate your credit score is a well-kept secret. Not only that, but each of the three agencies calculates your score slightly differently. This means your credit scores can be different across the three agencies.

Nonetheless, we do know the general factors they consider when calculating your credit score.

Type of credit providers that have made enquiries on your report;

The type of credit you have applied for;

Your repayment history;

The credit limit of each other credit products;

Negative entries;

The number of credit enquiries (credit applications) you have made.

When is a credit score used?

Credit providers, such as banks, lenders and other financial institutions, use your credit score to evaluate whether they should give you credit or lend you money. They use your credit score to determine how much of a risk you pose and decide whether you qualify for a loan or credit, how much interest they should charge you, and how high your borrowing limit should be based on your credit history.

Why is your credit score important?

With all of this in mind – why is your credit score important? There are several reasons why which we’ve outlined below.

Your credit score can help or hinder your application

Your credit score can be the difference between you being accepted or rejected for credit. If you are applying for a large loan and you have a below-average credit score, the lender you’re applying with might determine that you’re too risky of a borrower and reject your application.

A good credit score, on the other hand, could boost your application. If you have a strong credit history, then a lender might look at your application more favourably and approve your loan application.

This is one of the reasons why your credit score is important.

Interest rates

The interest rates you’re charged when you take out credit can end up costing you a lot over the lifetime of the credit. That’s why it’s a good idea to try and find loans, credit cards and other credit products with lower interest rates.

However, whether you can access low-interest-rate products can be heavily dependent on your credit score. Why is this? Lenders and financial institutions use interest rates as a way of protecting themselves against risk.

If you are deemed to be a risky borrower, then you will likely only be offered products with high-interest rates. That way, they get more money out of you quicker, so if you default on a repayment, they could already have a decent portion of the money they lent to you repaid.

This is another reason why your credit score is important – it can determine what products you’re offered and, if you have a good credit score, save you a lot of money in the long term.

Borrowing limit

Your credit score can also affect how much you can borrow. As with most things, it all boils down to risk. The bigger the loan, the bigger the risk could be for the lender should you default.

If you have a below-average credit score, then a lender might decide that it’s not willing to offer you a high borrowing limit and reject your application or only offer you products with lower borrowing limits.

However, if you had a good or higher credit score, then a lender could be willing to lend you larger amounts because you’re seen as less of a risk. This is how your credit score can influence how much you’re able to borrow.

What other factors do lenders look at?

It’s important to point out that your credit score is not the only factor that banks and lenders use to determine whether to lend you money. There are a range of factors they consider when making this decision. Nonetheless, your credit score is an important component of their decision.

Here’s what else they will likely consider:

Your bank statements – credit providers will typically ask for your bank statements from the past three months. This way they can get an insight into your spending habits and savings so they can see if you are responsible with your money.

Employment status and income – companies will want to ensure that you have reliable employment. Why? Because reliable employment infers that you are and will continue to receive regular income.

Government benefits – if you rely too much on government benefits then companies might not be willing to lend you money.

Gambling – do you gamble a lot? If so, this could be a red flag for lenders.

What is a good credit score?

A good credit score varies among the three CRAs. This is because they have different scales to rank your scores. Equifax measures your credit score on a scale from 0 – 1,200, Equifax, on the other hand, uses a scale of 0 – 1,000.

Each time you apply for credit, the company you have applied with will check your credit score. This is known as a hard enquiry and it lowers your credit score. Therefore, it’s a good idea to space out your credit applications.

Instead of applying for multiple loans and types of credit at once, you could instead do your research and make sure you meet the criteria before applying. You could also just make one application and wait and see if you are approved before going on to apply for other credit.

2. Make your repayments on time

Your repayment history contributes to a good chunk of your credit score. If you can show that you can make your repayments on time whenever you take on credit, then this will reflect positively on your credit report and boost your credit score.

On the flip side, if you miss your credit repayments frequently, then these will be listed as defaults on your credit report. Each time you default it will drag down your credit score. Not only that, but defaults stay on your credit report for up to five years.

This means each time you apply for credit in the next five years, every company you apply with will be able to see that you have previously defaulted on a payment. This will put you in the higher-risk category.

3. Check your credit report frequently

1 in 5 credit reports have some kind of mistake on them. This mistake could be an administration error, or it could be an indication that you’ve been a victim of identity theft.

Either way, mistakes in your credit report can harm your credit rating. That’s why it’s important to check your credit report frequently. That way you can identify a mistake early on and take the steps to remove the mistake.

4. Be consistent

Negative entries remain on your credit report for years. That’s why it’s important to be consistent with your good credit behaviour. One mistake can stay on your report for five years or more, and that mistake can affect your credit applications during this time. That’s why consistent positive credit behaviour can improve your credit score.

The verdict: Why is your credit score important?

To sum everything up, here’s why your credit score is important:

It could be the difference between you being accepted and rejected for credit;

It can determine your borrowing capacity;

It can affect the interest rates you’re charged (and either save or cost you money in the long term);

It can impact what utilities and phone plans you can access.

You are currently browsing the archives for the Credit Scores category.