Fraudsters are adopting more sophisticated methods to steal your card details. Tippla has put together a guide on how to protect yourself and your finances, and, if the worst should happen, report credit card fraud.

As technology advances, you don’t need to only worry about someone stealing your credit card out of your bag. But also that your details might be stolen online. So how can you protect yourself from and report credit card fraud if you do fall victim?

What is credit card fraud?

Let’s start by going over what is credit card fraud. As outlined by Experian, credit card fraud is “when someone uses your credit card or credit account to make a purchase you didn’t authorize”.

This could happen in many ways. A thief could steal your physical credit card and use it to make purchases. Alternatively, scammers could steal your details online, such as your credit card number, PIN and security code. With these details, they can make purchases online without having your physical card.

Types of credit card fraud

Credit card fraud comes in many shapes and sizes. Sometimes the fraud is physical, for example, they steal your credit card from your wallet, or the scam is online. This is referred to as card-not-present (CNP) fraud.

Here’s an overview of the different types of credit card fraud:

Credit card theft – when someone steals your credit card from your wallet, bag, car – wherever you keep it;

Using lost or stolen cards – say you dropped your credit card somewhere, and an opportunist picks it up. They proceed to use your card as if it was their own instead of reporting it to police;

Counterfeit cards – counterfeit credit cards are physical cards that were created with real account information that has been stolen from victims using a device called a “skimmer”. Often, the victims still have their real cards, so they’re not aware that their details have been stolen.

Intercepting and using mailed cards – when someone orders a new credit card and it’s sent to their address in the mail, fraudsters will steal this mail and use the card. Whilst credit card companies do their best to protect the cards during transit, they can be stolen from your mailbox.

Account takeover – as the name implies, account take over is when someone takes over your account. They could do this by getting your address and basic information and learn some of your security questions, such as your mother’s maiden name. Once they have this information, they’ll call up your bank or provider and change the account details. They might change the address, so a new card is sent to their address and not your own.

Fraudulent applications – using your details, such as your name, date of birth and address to apply for credit cards in your name.

CNP – card-not-present fraud is when scammers steal your details when you pay for something online. For this type of fraud, they only need basic information such as your credit card number and name to execute the fraud.

Credit card fraud in Australia

Although credit card fraud is an issue in Australia, there is an encouraging declining trend. According to figures released by the industry self-regulatory body Australian Payments Network (AusPayNet), fraud on payment card transactions dropped by 15.4% to $447.2 million for the 12 months to the 30th of June 2020. This continued the declining trend recorded in the previous year.

CNP fraud, which is when someone’s credit card details are stolen online and used in mainly online transactions, fell by 14.0% year-on-year down to $392.4 million.

Even though these figures are encouraging, that’s not to say that credit card fraud isn’t a real threat.

Credit card fraud vs identity theft

Identity theft is a type of fraud where someone uses another’s identity to either steal money or gain some kind of benefit. Credit card fraud is a type of identity theft. This is because the scammers are using your credit card details to make purchases without your consent.

As outlined by the Australian Competition and Consumer Commission’s (ACCC) scam statistics website Scamwatch, common methods of identity theft include phishing, hacking, remote access scams, malware and ransomware, fake online profiles, document theft and data breaches.

How to tell if you’re a victim of credit card fraud

The Australian Federal Police outlines the following ways you can identify if you have been a victim of identity theft:

- Items have appeared on your bank or credit card statements that you don’t recognise;

- You applied for a government benefit but are told that you are already claiming;

- You receive bills, invoices or receipts addressed to you for goods or services you haven’t asked for;

- You have been refused a financial service, such as a credit card or a loan, despite having a good credit history;

- A mobile phone contract has been set up in your name without your knowledge;

- You have received letters from solicitors or debt collectors for debts that aren’t yours.

How to report credit card fraud

Credit card fraud can happen even when your card is still in your wallet. Therefore, it’s a good idea to monitor your credit account to see if there are any suspicious transactions.

If you discover there are purchases on your credit account that you haven’t authorised, then you might be a victim to credit card fraud. If that’s the case, here’s what you should do:

Alert your credit card company

The first thing you should do if you discover you’ve been subject to credit card fraud is to immediately contact the credit card company and alert them to the fraudulent activity. They should put a hold on your account so the fraudsters can’t make any more purchases, and reimburse you the money.

Change your online passwords and PINs

Once you have alerted your credit card company or bank to the fraud, you should log into your account and change your online banking password and PIN. Password managers can help you create complex passwords that are hard for fraudsters to crack. You might want to consider using one of these to help create a strong password and prevent further fraud.

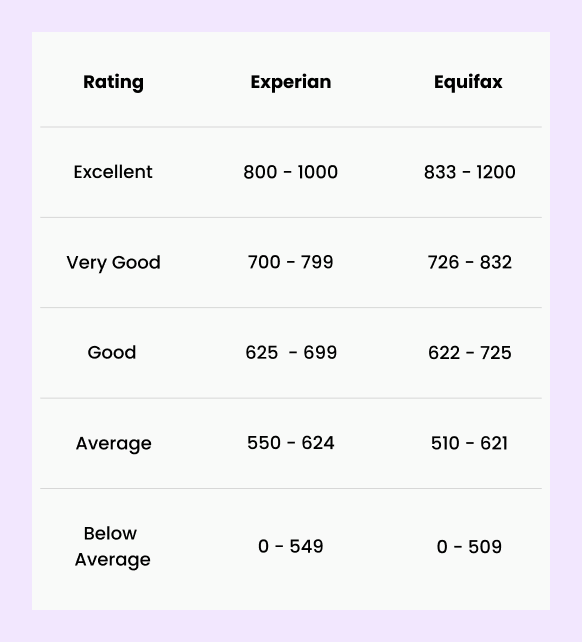

Check your credit report

Your credit report can be a valuable resource to help you detect credit card fraud and identity theft. Your credit report outlines all of the different credit accounts you have. If you check your report and see that you have credit accounts open that you never authorised, then you might be a victim of credit fraud.

If you have been a victim of fraud, then you should contact the three credit reporting agencies in Australia. These are Equifax, Experian and illion. You should report the fraud to each of these credit bureaus. You can ask them to place a ban on your consumer credit information.

Placing a ban on your consumer credit information can help prevent fraudsters opening accounts in your name. During the time the ban is in place, credit providers won’t be able to view your credit report without your written permission. Credit providers can’t open up an account without viewing your report.

You can also add a fraud alert to your credit report with each of the agencies. This means you will receive a notification when certain changes happen to your credit file.

Report credit card fraud to the police

If you are a victim of fraud, you should report credit card fraud to the police. If your details have been stolen online, you can report the fraud via ReportCyber on their website here. You can also call the following number: 1300 292 371.

How to protect yourself from credit card fraud

As the saying goes, prevention is better than cure. Here are some things you could do to protect yourself from falling victim to credit card fraud.

Keep your wallet or purse secure at all times

Whilst online scams are a real threat, thieves can still steal your credit card from out of your bag. When out in public, you should keep your wallet or purse secure at all times to stop it from being stolen.

Shred financial documents before putting them in the bin

The Australian Federal Police recommends shredding any personal or financial papers before you throw them away, so people can’t access your details. Alternatively, you should keep them in a secure place if you want to retain them.

Be careful when using your card

When you’re out in public, you should always cover the keypad at ATMs, to stop strangers from viewing your pin. The same goes for when you’re entering your pin on EFTPOS terminals.

You should also be aware of your surroundings and keep an eye out for anyone trying to watch you. Sometimes, scammers might try and attach technology to the ATM or EFTPOS terminal to scan your details. You should look out for any strange or loose fixtures attached.

For extra protection, you can ask your bank or financial institution for a credit or debit card with an embedded microchip. These are more secure than cards that only have magnetic stripes.

Be mindful of where you provide your details

When you’re shopping online, you should be mindful of where you provide your details. You should only buy from reputable companies or from ones whose security measures you can verify.

One method you can do is look at the company’s web address. With the https the “s” indicates that the site is secure.

On the other side of this, if you’re using a public computer, such as an internet cafe, or using an unsecured wireless connection (AKA a hotspot), avoid doing your internet banking or making payments.

Furthermore, you should be cautious of who you provide your personal and financial information to – both online and offline.

How can credit card fraud hurt your credit score?

Your credit report details all of your current credit accounts, as well as any credit you’ve had over the past two years. The impact fraud will have on your credit score, however, depends on what the scammer does with your details.

If they max out your credit card, this will hurt your credit score, as it indicates that you’re not responsible with your finances. If they make multiple applications in your name, this could also harm your rating.

However, it is important to highlight that although credit card fraud can hurt your credit score initially, once you alert the credit reporting agencies to the fraud, they will remove the fraudulent accounts or transactions and your credit score will revert to what it was.

Keep a watchful eye

Although credit card fraud might be on the decline in Australia, it remains a real threat for Aussies across the country. Even if you do all of the right things you could still become a victim to fraud. Constantly checking your accounts, prioritising your online security and knowing how to report credit card fraud could help you reduce the damage if your details are stolen.