If you understand your credit score, then you can utilise your credit rating to its full potential. However, it can be hard to find how credit scores in Australia work. That’s because an internet search can often produce results based on credit scores in the United States. Although there are many similarities between credit scores in Australia and the US, there are some key differences. Today, we’ll take you through what those are.

Credit bureaus in Australia vs the US

In Australia, the three credit bureaus are Equifax, Experian and illion. America also has three major credit bureaus – two of which you might recognise – Equifax, Experian and TransUnion.

We’ve already covered Equifax and Experian quite a lot here at Tippla, so we’ll introduce you to TransUnion. Operational in more than 30 countries, TransUnion is an American consumer credit reporting agency. The company collects and aggregates information for more than one billion individuals across the world.

In the US, credit bureaus perform a similar role to Australia. Specifically, the bureaus collect credit information, generate credit scores and reports, to allow credit providers to properly assess the risk associated with potential borrowers.

Credit Scores in Australia

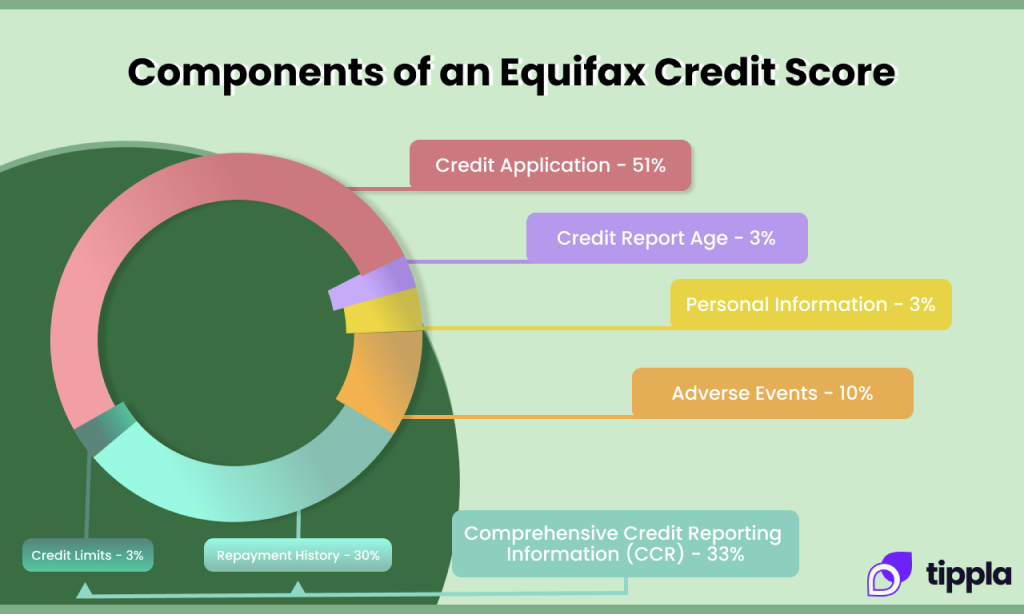

In Australia, you have three credit scores, one each from Equifax, Experian and illion. Credit scores in Australia are calculated by each of the bureaus using their own algorithms. Your credit scores are based on the information on your credit report.

This information includes:

- Credit accounts;

- Credit enquiries;

- Repayment history;

- Defaults;

- Negative entries.

Your credit score is one of the multiple factors used by credit providers to decide whether they will accept your application when you apply for credit (a loan, credit card, utilities, post-paid phone plan and more). They might also check your bank statements, employment status and eligibility, among other criteria.

Credit scores in the US

Although your credit score is important here in Australia, in the United States, it can carry a lot more weight. Furthermore, the credit bureaus across the pond have a system that they commonly use to calculate credit scores – Fair Isaac Corporation (FICO).

Whilst America also uses Comprehensive Credit Reporting (CCR), they do calculate credit scores differently, and some of the information they include on credit reports is different from how we do it in Australia.

Here are some of the things that go onto your credit report and make up your FICO score:

- Payment history

- Amount owed

- Length of credit history

- New credit

- Credit mix

Just like in Australia, the three CRAs in the US collect information differently. Therefore, American residents can have three different FICO scores, depending on which bureau they check with.

What are the differences between Australia and the US?

You already know a few differences already between credit scores in Australia and the US. But let’s look into the main differences a little deeper.

Credit utilisation

The credit utilisation rate (or ratio) is the amount of credit you have currently used divided by the total amount of revolving credit you have used. As an example, say you have a credit card with a limit of $10,0000, but you only spend $3,0000 every month, then your credit utilisation ratio is 30%.

In America, your credit utilisation rate carries a lot of weight when it comes to your credit score. However, in Australia, your credit utilisation ratio does not factor into the calculations of your credit score.

Credits score calculations

As we already highlighted, in the US, they mainly use the FICO system to calculate credit scores. In Australia, the bureaus do not use this system to calculate your credit scores.

Different scales are used

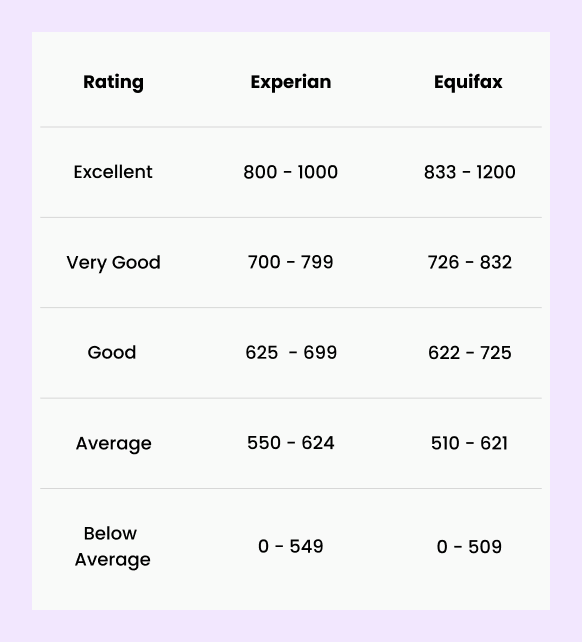

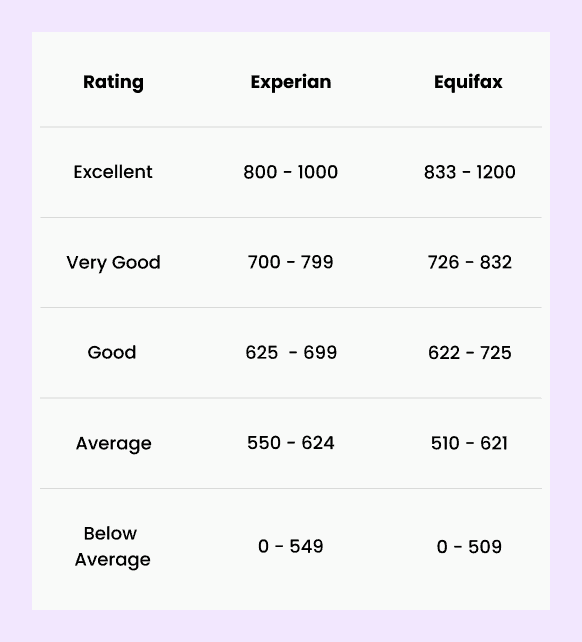

For credit scores in Australia, Equifax uses a scale ranging from 0 – 1,200 to rank credit scores. Experian and illion use a scale spanning from 0 – 1,000. The FICO system, however, uses a range of 300 to 850. On this scale, anything above 720 is deemed to be an excellent credit score.

Credit scores in Australia vs the US

Whilst there are some similarities between credit scores in Australia and in the United States – there are some key differences in the way credit scores are used and calculated. Because of this, when doing your own research on credit scores – be sure to check that you are looking at Australian resources. This way you know you’re getting the right information for you.

Does my Australian credit score count overseas?

Unfortunately, there isn’t an international credit score. Therefore, your Australian credit score won’t count if you move overseas. This means if you move overseas, you will need to build your credit history from scratch.

Credit scores don’t work the same across the world. Australia, the United Kingdom, Canada and the United States have similar credit scoring systems – but there are key differences between them. That’s why it’s a good idea to research what the credit scoring system is in whatever country you live in, to ensure you’re protecting your credit score.