“Budgeting isn’t about limiting yourself. It is about making the things that excite you possible.”

Introduction

“Budgeting” gives the impression that you have to deprive yourself of pleasure. It sounds like restricting yourself, taking away the fun of earning and spending. Let’s change the way we think about money and call it your financial master plan.

You might be surprised: you don’t have to live a boring life to grow your savings and get your spendings under control. However, many Australians spend their money without consciously choosing where their money actually goes. There is true power in knowing your (sometimes bad) spending habits and making sure you still indulge but in the right places. The key to a good budget is to identify which areas your money is currently going to and to analyse if that’s what you actually want to spend your money on.

In this lesson, you will learn:

- About the true power of a financial plan;

- How to shift bad habits;

- What you can use a transition budget for;

- Which saving strategies you can use to grow your money.

Setting a realistic plan

It’s happened to all of us at least once: you had really good intentions to save a big chunk of your income but somehow, this money disappeared into a big brunch with your friends, plenty of takeaway coffees, or a present to yourself. Your financial master plan might be the key to helping you reach your financial goals – however, it should still be fun and spark joy!

Do you want to grow your savings, but you still want to enjoy life to the fullest? Even if you are on a tight budget, you could still save good money by making a few small changes.

Be brutally honest with yourself: Unhealthy spending habits

Do you know what’s draining your bank account? Often, it’s not actually that one big thing that you really wanted to get, it’s everyday habits that often stay unnoticed. When you are assessing your financial situation, you have to be brutally honest with yourself. Where does your money actually go? Try and take a week or two and write it all down. And with all, we mean everything! That Snickers bar on the way home, the morning coffee, the cheeky Maccas after a night out.

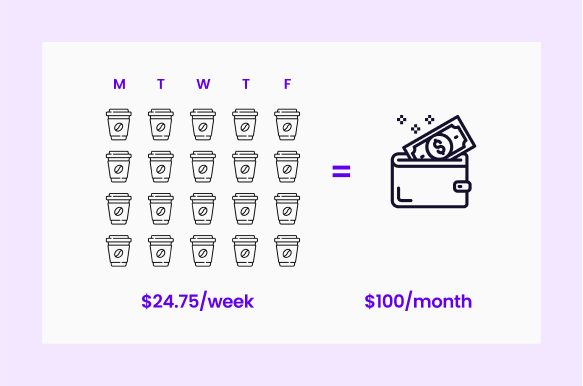

Your takeaway morning coffee is a great example: if you buy a coffee on your way to work every morning and said coffee is $4.95, you spend $24.75/week on coffee. Doesn’t sound too bad? That’s almost $100 per month! Of course, we are not suggesting to scratch your morning coffees out of your life – but it’s good to be aware of it.

To track your finances, you could use a good old spreadsheet if you prefer the classic way. Alternatively, you could go digital and find an app that integrates your bank accounts and automatically categorises your spendings. It’s time to check your financial health!

Identify bad habits and make micro changes

We are no saints! This is not about perfecting your spending habits, it’s about taking control. Say you have identified that you spend way too much money on said morning coffees – you don’t have to go to the full extreme and not spend money on coffee AT ALL. Rather, try and set yourself a realistic coffee budget. Instead of $100, maybe spend $50 and bring your own coffee every other day. You don’t have to change your behaviour completely, instead make better choices and embrace it when you allow yourself to indulge. This way, “bad” habits can easily be turned into a saving opportunity.

Use apps to stay on top of your budget!

The key to successful savings is consistency. You don’t need to put away big chunks of money to grow your savings. Instead, make every penny count! Apps like Pocketbook support you with reaching your savings goals by setting budgets over multiple bank accounts. You could categorise your spendings and keep track records of any bad habits you may have. Additionally, round-up apps like Raiz make your change work for you. They use spare change from any purchases and help you grow it through portfolio investments.

Make a transition budget

Do you want to move towards spending less money in the long run? Some people go to extremes and commit to a month of non-spending to reset their personal habits. If that’s just not your cup of tea, you could see if a ‘transition budget’ might be better instead. By changing your budget gradually over the next couple of months, you could change your spending habits in a more sustainable way instead of asking for a habit change straight away.

So how can you do this? Try and work out your goal budget and then use a time period, say six months, to move towards this budget. Therefore, you don’t create just one, you create six realistic budgets towards your dream budget. But don’t forget to still accommodate your actual needs such as rent and bills. These parts of the budget won’t change while other parts may be more flexible.

Before jumping into making a budget, do your research and determine which course of action is best for you. These are only suggestions and not advice.

50-20-30 Budget

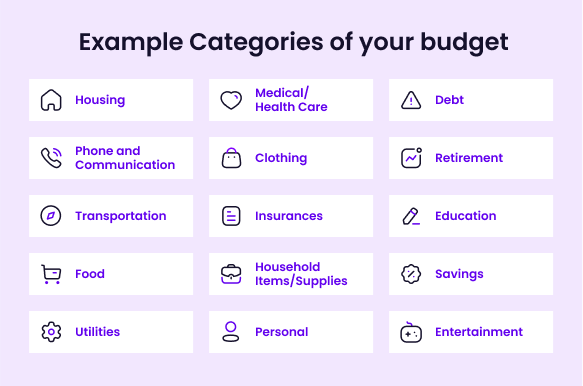

The general idea of a 50-20-30 budget is to split your income into three different categories. The first category is needs, which covers everything that is non-negotiable. Payments like rent, groceries, utilities and transportation would be considered needs. Wants includes fun items and events that you splurge on, and savings is probably self-explanatory!

This is how you would split your income into the following categories if you chose a 50-20-30 budget:

50% in Needs

20% in Savings

30% in Wants

By the end of each month, anything that is leftover in wants and needs should be transferred into savings. Each month starts with a fresh budget.

Automate your savings

Saving money is much harder if you let the money sit in your personal account, looking like it could be spent. Why don’t you try and nominate a certain amount and automatically transfer it to a savings account right after payday? This could eliminate the false feeling of having more money to spend than you actually should and helps you grow your savings without having to do anything.

It doesn’t have to be a huge amount. Instead, you could set a realistic savings goal and save towards it. If you put $50 into savings each fortnight, you save $1,300/year.

Developing an emergency fund

Life doesn’t always go to plan as we all have had to learn with the COVID-19 pandemic. You might sleep much better at night knowing that you’ve got your own back in case of an emergency. Having enough money in your bank account to cover your expenses for a while should take a huge weight off your shoulders.

You don’t have to rush. You could just set up a savings account and slowly save towards your goals. If you want to take it easy, start with the goal of saving one month of income as a safety buffer. Once that is achieved, save your way towards three months.

Negotiate a better interest rate for your credit cards

Credit cards tend to come with high interest rates. While this doesn’t matter if you always pay them off on time, you could try to get a better deal wherever you can.

Most people don’t know that you can actually negotiate the interest rate on your credit cards with your provider. Especially if you have a good credit score and a solid repayment history with a certain company, they could offer you a better deal if you ask. Even if they don’t, it could be worth trying.

Make money an easy conversation

Talking about finances can be uncomfortable, especially when you are on a tighter budget than your friends or partner. However, it doesn’t have to be. We are all in different places in life and if your friends keep inviting you to this fancy restaurant for dinner that’s just a tad too expensive for you, you should let them know. Honesty could pay off both for your finances and in your friendships. Real friends would rather know than make you feel uncomfortable and overspend. If it’s not common in your group of friends, be the first one to make money an easy conversation. Having open conversations about finances can be very empowering and you can share some of your new knowledge with your friends!