“Success is not an accident. It is actually a choice.”

Stephen Curry

Tippla is a tool that helps Australians to access and understand their credit scores. We are not financial advisors. We work with a range of industry professionals and compliance check our content to ensure factual accuracy. We do not provide professional financial advice. Consider seeking independent legal, financial, taxation or other advice to check how the information in this lesson relates to your unique circumstances.

Introduction

Welcome to Tippla’s Credit School, a short online course where you’ll learn all you need to know about your credit score. We’re so happy to have you with us and we’re stoked that you’re taking this step towards achieving financial wellbeing.

In this online course, you’ll venture through six individual lessons which will guide you through all of the nuances of a credit score: what is a credit score, what goes into your credit report and more. You’ll learn all you need to know about credit scores.

Before we get stuck into the lessons, there are two things you need to know. Firstly, what is credit? As defined by MoneySmart: “Credit is money you borrow from a bank or financial institution. The amount you borrow is debt. You will need to pay back your debt, usually with interest and fees on top.”

Examples of credit include:

- Credit card;

- Loans – personal (secured and unsecured), car, mortgage, business, student and more;

- Buy Now Pay Later services;

- Mobile phone;

- Internet;

- Electricity or gas;

- Water.

Secondly, what is a credit score? One thing is for sure – it’s an important number to know! A credit score, or credit rating, is a number ranging from 0 – 1,200, and it is part of the information credit providers, such as banks, finance companies and utility providers use to assess when someone applies for credit.

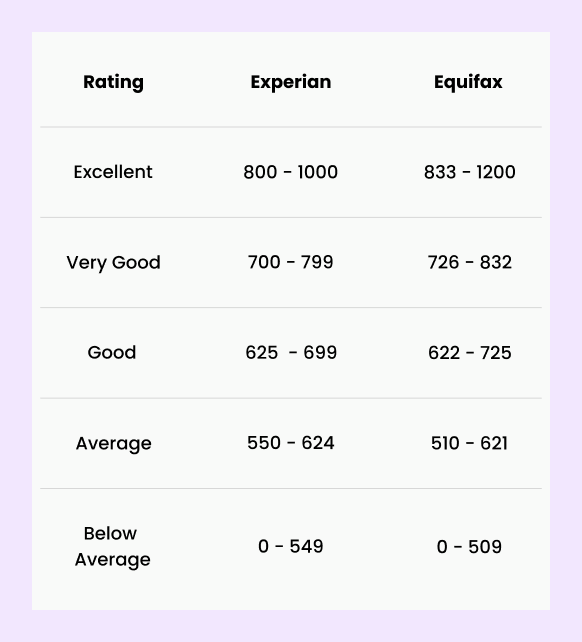

Your credit score is based on a five-point scale: excellent, very good, good, average and below average. A credit score acts as a guide for credit providers to assess how risky a borrower you are.

If you have a good, or even excellent credit score, that generally means you have a history of being responsible with your debt. If your credit score is less than ideal, that indicates to a borrower that providing you with a credit facility is more of a risk. Because of this, if you’re trying to apply for a credit card or a loan, for example, you will likely be given products with higher interest rates and less ideal terms, as opposed to someone with a good credit rating.

It’s fair to say that your credit score is an important number! If you didn’t know anything about your credit score before joining Tippla, you’re not alone! 73% of Australians don’t know their credit scores or why they are important. But we at Tippla believe it’s time to make a change. So, let’s get stuck into it!

What is a credit score?

We already covered the basics of what a credit score is in the introduction – it’s a numerical representation of your creditworthiness. Knowing your credit score, and knowing what goes into them, could help you negotiate better deals with your existing credit facilities, or when you’re applying for new credit.

Your credit rating is based on a number of factors such as previous repayment history, how many credit accounts you have or have had in the past, and if you normally pay your bills on time.

Previously, this was only based on so-called negative reporting. If you missed a payment, the company would report to the credit bureaus and a negative entry would appear on your report. Since 2018, Australia uses Comprehensive Credit Reporting (CCR) which now includes positive behaviour being reported to your account. While not all rental agencies and utility providers report to credit bureaus just yet, it is likely to become more common in the future.

Why do I have two credit scores?

So now you have a better idea of what a credit score is, but what you might not know, is that you actually have more than one credit score. In Australia, there are three credit reporting agencies (also referred to as credit bureaus) – Equifax, Experian and illion. That means you have not one, not two, but three credit scores and reports!

Each of these reporting agencies has different reporting algorithms and they have access to different streams of information. Because of this, it is highly likely that you will have a different credit score for each of these credit reporting agencies. Sometimes, there can be a big difference, and other times, the change in ratings from each agency is minimal.

On Tippla you can see two of your credit scores – one from Equifax and one from Experian.

What is a good credit score?

Again, a low credit score doesn’t mean you can’t apply for credit. But it limits your options, and in some cases, may even mean that a credit provider rejects your application. The good news: your credit score changes over time and positive actions should slowly help build it up!

How is my credit score calculated?

There are a number of factors that contribute to your credit score. Generally speaking, your credit score is based on what’s in your credit report. However, the information listed on your credit report varies between the three credit bureaus. They each have their own style of reporting as well as their individual algorithms and priorities which calculate your credit score.

We’ll go into more detail about what your credit report is, and what goes into it in our next module, but some of the general factors that affect your credit score are:

- How much money you’ve borrowed;

- Whether you made your repayments on time;

- How many credit enquiries you’ve made, and if you made them in quick succession.

The true impact of credit scores

A lot of people assume their credit score only affects them when they apply for finance? This is false! Your credit score can enable or hinder you in multiple areas of your life. In fact, there are many reasons why your credit score is important. Applying with a rental agency can be a tough game when you have bad credit and once you get accepted, you may have to put down a security deposit for utilities if you are considered a risky candidate.

The benefits of a good credit score include:

- No security deposits on utilities such as phone bills and electricity;

- Easier approval for rentals and apartments;

- Better rates on car insurance;

- Better chances of approval for a mortgage;

- Access to better credit cards with lower interest rates;

- Better availability and rates for loans;

- Access to refinance for loans and debt consolidation options.

Is my data safe?

Your credit score contains sensitive information. Research has shown that one-third of Australians never talk about finances. More than that, most people don’t want their financial information out there for everyone to see!

So, can just anyone request access to your credit report? Definitely not! Your data security is regulated in The Privacy Act from 1988. Only specific Government organisations and businesses authorised by you will be able to access your credit score. Each time a company sends an enquiry to see your data, it will be logged on your credit report. You can see them under the tab “Credit Enquiries” on your Tippla dashboard. Any organisation handling your credit score data (like Tippla) has to follow the same regulations.