Introduction

Your credit report contains in-depth information about your credit accounts and your previous payment history. The unique formula your credit score is made of is a well-kept secret. However, we do know what’s listed and a general idea of how much each section weighs on your credit score. When you request to see your credit report, you may see different information from what a potential credit provider would see. For example, for security reasons, you can see who accessed your credit report and when – credit providers can’t see this information.

Mistakes happen – every fifth credit score contains an error. And wrongly listed information could cost you valuable points. That’s why it’s important to check your information frequently to catch mistakes early on.

Credit report vs credit score

Your credit score is based on your credit report, they are not the same thing! A credit score is a 4-digit number that indicates your creditworthiness. It is calculated by looking at your credit report that contains detailed information about previous and current credit accounts, your repayment history and any so-called adverse events (negative entries) that are listed on your credit report.

If you speak about your credit score, you are referring to your number. Your credit report, on the other hand, contains more information and some credit providers calculate your creditworthiness based on other factors in there.

Be aware: 1 out of 5 credit scores contain at least one mistake that can cause your number to drop. It’s important to check your information thoroughly and frequently.

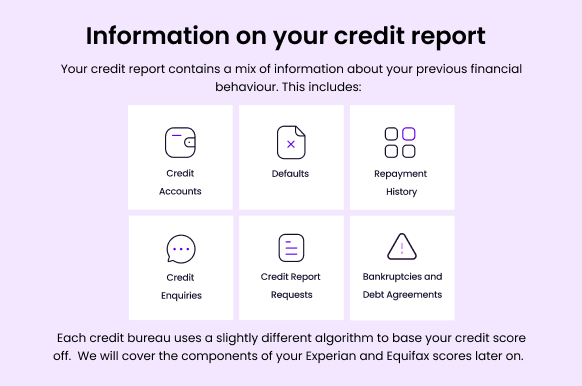

What goes into your credit report?

Again, what goes into your credit report varies across credit bureaus. Here is an overview of what goes into your Experian and Equifax credit reports.

Your Experian Report

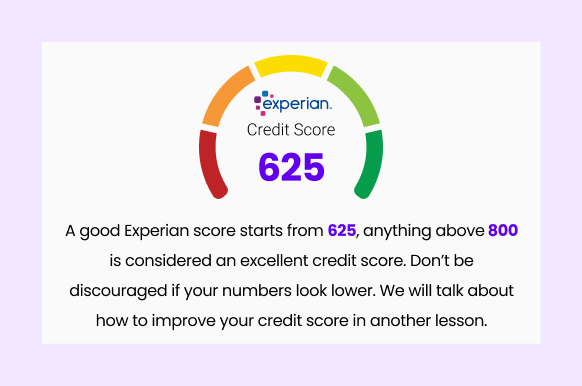

Your Experian credit score goes up to 1,000. However, if your number only has 3 digits, that’s absolutely normal. Almost no one can get a perfect score, and a good credit score means that you manage your debt better than the average person, a great starting point!

Experian states that the main contributing factors for your Australian credit score are credit history, credit accounts, credit limits, and credit enquiries. The value of a piece of information also changes over time. Accounts that have been open for longer may have a higher weight because they showcase your credit behaviour over a more significant period of time.

Your Experian report lists:

- Personal information like your name, DoB, gender, address, drivers licence and known addresses;

- Your Experian Credit Score;

- Current credit providers;

- Credit enquiries (AKA credit applications. Experian calls them file records but it’s the same thing);

- Defaults and serious credit infringements;

- Credit history;

- Public information;

- Personal statements*.

Source: Experian

*Under certain circumstances, Experian allows you to write a short personal statement to explain that you may be a victim of identity theft while the issue is being resolved. Alternatively, you can put a short-term ban on your credit report to protect it from damage.

Your Equifax Report

Your Equifax score is a number between 0 and 1,200. With your credit score, you want to aim high but don’t stress yourself too much. A good credit score could already open many doors when applying for finance.

Your Equifax score is based on your Equifax credit report and this report changes whenever a new piece of information is added or old information gets removed. Therefore, your score can change frequently, sometimes multiple times per day.

Your Equifax report lists:

- Type of credit provider (there are different risks associated with different credit providers and industries. It is much easier to get an in-store credit card vs. a personal loan from a bank);

- Type and size of your credit;

- Number of credit enquiries and if you have been shopping around for credit applications (this may indicate a higher risk);

- Directorship and proprietorship information;

- Age of credit report;

- Personal details;

- Default information;

- Court writs and default judgements.

Source: Equifax

Identity theft and fraud

In a worst-case scenario, someone steals your credit card details or even worse, your full identity. A fraudster can use your credit card on your behalf, eat into your savings or leave you with unpaid bills for purchases you didn’t even know about. Accumulation of credit enquiries and unpaid bills can seriously harm your credit score. Luckily, Equifax and Experian both offer support and will help you resolve this issue. You can even ban your credit report for the time your case is being investigated to protect it from further harm. However, it will take some time and effort from your side. On a good note: your credit score should recover immediately, once the issue is resolved!

You should check your credit report frequently for any irregular entries or any changes that you don’t recognise. Once spotted, you should act immediately, to start the process early.

Wrong information on your credit report

If you spot something wrong with your credit report, you should take action. Mistakes in your credit report can be a major cause of a lower credit score. Luckily, there is a solution. You should thoroughly scan through your credit report every so often and make sure that you recognise everything that is listed and that all information is correct. Even minor mistakes like a typo in your address can cause duplicated content or even a separate conflicting file.

Experian – Request a correction

When going through your credit report, you should look out for:

- Is your name spelt correctly?

- Are your last two addresses listed?

- Are all loans listed on your report only listed once?

- Are the listed repayments correct?

- Is the balance for each account listed correctly?

Please keep in mind that credit providers such as banks, lenders and more, only report to the credit bureaus once per month. Therefore, the data may not reflect in real-time what payments you have made.