Introduction

When it comes to credit scores and credit reports, it’s important to know that they don’t work the same in every country. A typical Google search for information about credit scores and reports will often yield many results tailored to the United States. However, whilst many things are similar in Australia and the United States, there are some key differences that you should be aware of.

Specifically, we will cover:

- Who are the credit bureaus in the United States?

- What are the differences between credit scores and reports in the US and Australia?

- What is a FICO credit score?

- Does a FICO score matter in Australia?

Who are the credit bureaus in the United States?

There are three main credit bureaus in the United States, two of which, you might recognise!

The three credit bureaus are:

- Equifax

- Experian

- TransUnion

You already know about Equifax and Experian, so we’ll tell you a little bit about TransUnion. Although operational in more than 30 countries, TransUnion is an American consumer credit reporting agency. The company collects and aggregates information for more than one billion individuals across the world.

These three credit bureaus perform a similar role to the CRAs in Australia. They collect credit information, generate credit scores and reports, to allow credit providers to properly assess the risk associated with potential borrowers.

Credit scores in the US

Whilst your credit score is an important number here in Australia, it is one of the multiple factors used to determine your creditworthiness. In other countries, such as the United States, your credit score can carry a lot more weight.

Equifax, Experian and TransUnion use the data provided to them to create a Fair Isaac Corporation (FICO) score. The FICO system is the most commonly used system to calculate credit scores in the country. Simply put, FICO score = credit score in the US.

Like Australia, the US has a comprehensive credit reporting system in place, so not only negative entries are included in your reports, but also any positive information as well.

Specifically, here are some of the things that go onto your credit report and make up your FICO score:

- Payment history

- Amount owed

- Length of credit history

- New credit

- Credit mix

Just like in Australia, the three CRAs in the US collect information differently. Therefore, American residents can have three different FICO scores, depending on which bureau they check with.

What are the differences between Australia and the US?

Specifically, there are a few standout differences between Australia and the US. Here’s what they are:

Credit utilisation

Your credit utilisation rate, or ratio, is one of the main ingredients which goes into calculating US credit scores. Your credit utilisation rate is the amount of revolving credit you have currently used divided by the total amount of revolving credit you have available to you. Put simply – it’s how much you owe divided by your total credit limit.

As an example, save you have a credit card with a limit of $10,0000, but you only spend $3,0000 every month, then your credit utilisation ratio is 30%.

Whilst, generally speaking, having a low credit utilisation ratio is good, because it means the amount you owe isn’t too high – when it comes to Australia, this does not factor into your credit score.

The way credit scores are calculated

Whilst the algorithms the credit bureaus use is a well-guarded secret, and there’s a lot of crossover between the information used to calculate Australian and US credit scores, they are calculated differently.

Specifically, in the US, the FICO system is the main system used to calculate your credit score. In Australia, we do not use this system to calculate credit scores.

Different scales are used

Not only does some information matter in the US, where it doesn’t in Australia, the scales used between the two countries are different. For example, in Australia, Equifax uses a scale ranging from 0 – 1,200 to rank credit scores. Experian and illion use a scale spanning from 0 – 1,000.

The FICO system, however, uses a range of 300 to 850. On this scale, anything above 720 is deemed to be an excellent credit score.

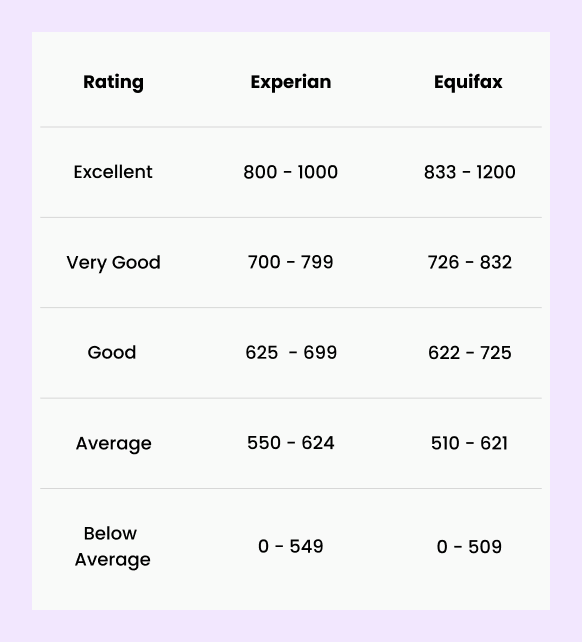

In Australia, here’s how Equifax and Experian categorise credit scores:

Source: Equifax and Experian

Similar but different

So there you have it. Whilst there are many similarities between Australia and America’s credit scoring systems, there are some key differences. It’s important that you’re aware of these differences when doing your own research.