“Good debt is a powerful tool but bad debt can kill you.”

Robert Kiyosaki

Tippla is a tool that helps Australians to access and understand their credit scores. We are not financial advisors. We work with a range of industry professionals and compliance check our content to ensure factual accuracy. We do not provide professional financial advice. Consider seeking independent legal, financial, taxation or other advice to check how the information in this lesson relates to your unique circumstances.

Introduction

Debt, almost everyone has it but no one likes to talk about it. In 2016, the average Australian household debt was $168,600, with 29% of households holding more debt than they were able to repay. Debt has a bad reputation, however, there are different types of debt.

So why are we talking about debt? As we covered in our first lesson, credit is when you borrow money from either a bank or a financial institution. The amount that you borrow is debt. Effectively managing this debt could be the difference between a good and bad credit score, and the difference between being financially stable or struggling to make repayments.

We want to change the way we speak about debt and openly address issues that are so important to speak about! Whilst we at Tippla will never advise you to take on debt, we do want you to know the subtleties of debt.

In this lesson, you will learn:

- Why not all debt is “bad”;

- How to spot bad debt;

- If you accumulated too much debt;

- How debt may affect your credit score.

What’s the difference between good and bad debt?

40% of Australians experience financial distress, according to NAB Australian Wellbeing Survey for Q4 2019, while most Australians take on some form of debt during their life.

However, having debt does not mean you are in financial distress, as not all debt is the same. Under certain circumstances, taking on debt could be a good idea and an important investment in your future. Whether the debt is good or bad could be measured in its consequences.

Before taking on any type of debt, it is worth talking to a financial advisor, who will be able to take a look at your financial situation and determine whether taking on a certain type of debt is in your best interests. Furthermore, the Australian Securities and Investments Commission (ASIC) also outlines all the things you should check before taking on any type of credit.

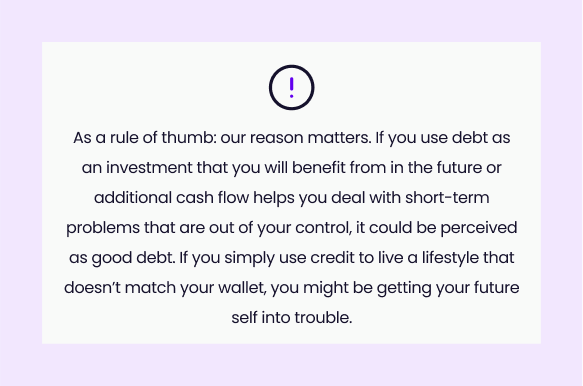

When you’re considering whether to apply for credit, you should ask yourself the following: is your debt a short-term fix for a long-term problem or an investment into future value?

To give you an example, when you take out a mortgage to buy a home, repaying your debt is a long-term commitment over many years. However, over time, it is expected that your property should increase in value and you can either reduce your own living expenses, rent or sell it for financial gain. And while you are repaying your mortgage, your home’s worth in equity increases and gives you additional borrowing power. This is an example of what could be considered as positive debt.

On the other hand of this example, if you get in debt to buy a bigger TV for your living room and struggle to make the repayments, you are making your life harder and don’t add any value to your future. In fact, it’s quite the opposite, you exchange short-term fun for potential long-term stress and worries. This could be an example of so-called “bad debt”.

Nonetheless, a mortgage is not always considered good debt. If you buy a house that is out of your price range, for example, then it might not have been the best decision for you. That’s why it’s important to speak with a financial counsellor if you are ever unsure.

When taking out credit, you should be aiming for:

- A low-interest rate;

- It will add future value;

- Affordable to repay.

What you should try and avoid:

- High-interest rate;

- Debt that adds stress to your future life;

- Debt that you struggle to repay: when the cost of borrowing is higher than the amount you’re able to repay each month.

How does debt affect your life?

Taking on debt could be an empowering step towards a richer future or a major downer, depending on where you are at in life. It can affect you in many different ways.

Financial effects of debt

Taking on debt means committing to frequent repayments over an extended period of time. In the case of a mortgage, this can be 25 – 30 years. Therefore, it is important to find yourself in a position of financial stability. Will you be able to comfortably make your repayments every week, fortnight or month?

Taking on too much debt could cause financial struggles and may prevent you from being able to access additional finance options that you may want or need. Why so? Taking out the maximum amount of credit you can possibly borrow may affect your credit score. Potential credit providers may assess you as a riskier borrower because you already borrowed a big sum of money. This might make you less likely to receive approval on other credit applications.

Tippla hint: Want to know if you can comfortably make repayments for a potential debt? You might want to do a budget before taking out any type of credit. This way, you could try to determine whether you could easily make the repayments and ensure you are taking on good debt.

Health effects of debt

You don’t need to lose sleep over well-managed debt. However, if you find yourself in a sticky financial situation, this can cause high blood pressure, sleepless nights, anxiety and other stress-related issues. If you are unsure whether you are putting too much financial pressure on yourself, it’s best to contact a free financial advisor prior to any loan application. They can talk you through realistic plans on how to manage your debt better and even improve your situation if you are already committed to a stressful amount of debt.

Debt and relationships

Financial stress has been identified as one of the key problems in relationships. Working towards your financial goals in harmony is empowering and a beautiful feeling. However, poorly managed debt may create additional stress for you and your partner and cause uncomfortable arguments.

What to do if debt gets out of hand

While we at Tippla will always do our best to provide you with the information you need to financially thrive, it’s important to note that we’re not debt counsellors, nor do we provide financial advice. Be sure to speak to your financial services professional before making any decisions.

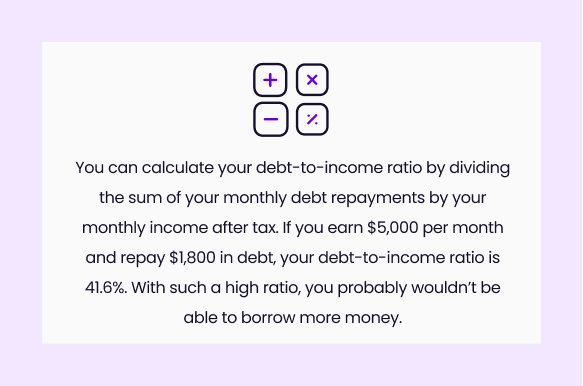

Your debt to credit ratio

A good indication of whether you have taken on too much debt is your debt-to-income ratio. While having debt, in general, isn’t a problem, you should keep an eye on the amount.

Each credit account has a maximum amount of credit you can take. All credit accounts combined add up to the maximum amount of credit you have access to at the current time. While it is not the most important factor in your credit report, future credit providers can assess how much use you are making of your existing credit already and how this could affect your ability to repay. In short, the more credit you take out at the same time, the more likely you are to potentially struggle to repay additional credit.

If you have taken on too much debt and it feels overwhelming, there are options for help. There are many ways on how to tackle debt fast and most credit providers have systems in place to support you if you are experiencing hardship or struggle to make your repayments. Reach out for support. Each case is different and a counsellor will provide advice on what’s best in your personal situation.

Debt and credit scores

As contradictory as it sounds – debt isn’t necessarily negative for your credit score. Your credit score is a numeric display of how well you can manage debt.

Well-managed debt indicates to future credit providers that you are able to manage multiple debts at once while sticking to your repayment dates.

Tippla tip: You can use Tippla as your debt overview service! On Tippla, you can check all of your credit facilities in one place, see what your total amount owed is and your total monthly payment.

Missing payments

Life doesn’t always go to plan. You may have a change of circumstances and are suddenly not able to meet your repayment obligations. A listed missed payment or default will stay on your credit report for up to 5 years and can seriously harm your credit score. Additionally, penalty fees may occur for late payments that impact your personal finances and increase your debt even further.

However, credit providers generally have procedures in place to help you if you are struggling. So if you find yourself in difficult times, it might be in your best interest to reach out to your lender for assistance.

Bankruptcy

The ins and outs of bankruptcy can be confusing. How bankruptcy affects your credit score can be even trickier to understand. So, we wanted to break this down for you.

As explained by the Australian Financial Security Authority, the government agency that manages bankruptcy for individuals, bankruptcy is the legal process when you’re declared unable to pay your debts.

When you’re declared bankrupt, it can release you from most of your debts. You can also be provided relief once being declared bankrupt, to give you the opportunity to make a fresh start. However, if you had a loan that was secured by an asset, the credit provider can start the process of repossession of the secured asset to recover part or all of the debt owed.

There are two ways in Australia to enter into bankruptcy. You can either enter into voluntary bankruptcy by completing and submitting a Bankruptcy Form. Or, a creditor can petition to have you enter a bankruptcy agreement through court proceedings, referred to as a sequestration order.

Bankruptcy normally lasts for 3 years and 1 day.

Bankruptcy and your credit score

Whilst declaring bankruptcy can give you the chance to start over again, it can still have a severe impact on numerous aspects of your life. One of these could be your ability to obtain credit.

In Australia, for anything above $5,788, you must disclose that you are bankrupt or in a debt agreement before you can buy goods or services on credit. After your bankruptcy has ended, all restrictions on applying for loans or credit are lifted. Then, it’s up to the credit provider to decide if they will lend you money.

However, your credit report will still show your bankruptcy even after it has ended. Specifically, your report will show your bankruptcy for either:

- 2 years from when your bankruptcy ends or;

- 5 years from the date you became bankrupt (whichever is later).

Therefore, bankruptcy will remain on your credit report for a maximum of 5 years, assuming your bankruptcy period lasts for 3 years and 1 day. The bankruptcy status will change on your report depending on whether you completed the agreement within the 5 years.

What is important to highlight here is that it is completely up to the credit provider as to whether they will give you a loan. The bankruptcy indicates to them that you are not able to effectively manage your debt and you are a high-risk borrower.

Whilst it’s likely that each credit provider has different criteria that determine whether they will lend to someone who has been bankrupt, there are some things that you can do that might help your situation.

If you can show that your financial situation has changed and you are now able to effectively manage your debt and have overcome your bad habits, this could go a long way for a creditor.

However, it’s probably in your best interest to avoid bankruptcy altogether. Most credit providers have systems in place to support you if you are experiencing hardship or struggle to make your repayments. You can also reach out for support. Each case is different and a financial counsellor will provide advice on what’s best in your personal situation.

How much does bankruptcy hurt my score?

The exact ingredients that go into a credit score are well-guarded secrets of credit bureaus, so no one knows exactly how they calculate your credit score. However, what we do know is that if you go into bankruptcy your score will be negatively impacted.

Once you start the process, your credit score will then be adjusted depending on whether you complete the bankruptcy agreement within the maximum period of 5 years. A standard period for completing a bankruptcy agreement is 3 years and 1 day, whereby it will remain on your credit file for an additional two years.