Can You Get a Personal Loan After Bankruptcy?

This text can be used to describe shortly what the Credit Score Basic is used for.

Have you recently been through the bankruptcy process and you’re wondering if you can now get a loan? Tippla has put together this helpful article so you can understand your options.

There are many reasons why someone might have to enter into bankruptcy. If you are about to enter into bankruptcy, or you’ve just come out of the bankruptcy process, can you still get a personal loan after bankruptcy? We’ve gathered all the information to help you understand your options.

Bankruptcy in Australia

Bankruptcy is the legal process that is declared when someone is unable to repay their debts. If you are struggling to repay your debts, there are three formal options available for you – bankruptcy, personal insolvency agreements and debt agreements. Today, we’re going to focus on bankruptcy.

Bankruptcy typically lasts for 3 years and 1 day, however, you can end your bankruptcy earlier if you’re able to repay your debts within this time. Bankruptcy can remain on your credit report for up to 5 years.

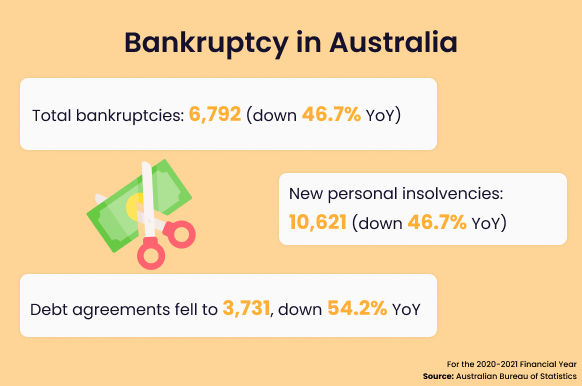

According to the Australian Financial Security Authority (AFSA), there were 6,792 bankruptcies in Australia in the 2020-2021 financial year. This was 46.7% less than the previous financial year.

Going through bankruptcy

If you need to enter into bankruptcy, there are two ways you can do so. According to the AFSA: “You can enter into voluntary bankruptcy. To do this you need to complete and submit a Bankruptcy Form. It’s also possible that someone you owe money to (a creditor) can make you bankrupt through a court process. We refer to this as a sequestration order.”

When you enter into bankruptcy, the Australian government will appoint you with a trustee, who is a person or body who manages your bankruptcy. When you enter into bankruptcy, you are obligated to do the following:

- Provide details of your debts, income and assets to your trustee;

- Your trustee will notify your creditors that you have entered into bankruptcy. This will prevent most creditors you owe money to from contacting you regarding your debt;

- Your trustee may sell some of your assets to repay your debts;

- If your income exceeds a certain amount, then you may need to make compulsory payments.

Before entering bankruptcy

If you are currently struggling with your debts, there are a few things you can do before formally entering into bankruptcy.

Seek financial advice

In Australia, there are free resources you can use to help you get on top of your debt, but it’s important that you act quickly. You can reach out to the National Debt Hotline, a not-for-profit service that helps Australians tackle their debt problems. You can also speak to a free financial counsellor through their service.

By using the National Debt Hotline, you can speak to a professional who can help you get on top of your debt before it escalates to bankruptcy, or they can help you understand your options if you need to enter into some kind of debt agreement.

Reach out to your creditor

As soon as you begin to struggle with making your loan repayments, it’s important that you reach out to your creditor/s. You can let them know that you are experiencing financial difficulty. Many credit providers have hardship programs in place that have been created to help support their customers during times like these.

Specifically, you might be able to agree with your creditor on extending your repayment period, set up a flexible payment arrangement and more. However, some of these options could be legally enforceable. Therefore, you may want to seek independent advice before committing to anything.

Accessing finance during bankruptcy

If you have entered into bankruptcy – what are your options when it comes to finance? We have broken this down into two parts – accessing finance when you’re going through the bankruptcy process, and whether you can get a personal loan after bankruptcy.

Can you get a personal loan during bankruptcy?

Let’s start first with whether you can get a personal loan during bankruptcy. Technically, the answer is yes, but there are a few things you need to be aware of. In Australia, according to the Bankruptcy Act of 1996, Section 269 you will have to disclose your bankruptcy status as a debtor if you want to borrow more than $3,000. If you don’t disclose your bankruptcy, then you could face imprisonment.

If you apply for a loan when you’re in the bankruptcy process – this is a big risk for a lender. This is because bankruptcy suggests that you are not effectively able to manage your debt and you are, therefore, a high-risk borrower.

Whilst you can still apply for a loan when you’re bankrupt, it is completely up to the lender as to whether they will loan you money. In order for them to accept your application, you will typically need to prove that your situation has changed since entering the bankruptcy process.

This could include securing employment when you were previously unemployed, adjusting your lifestyle to one that you can comfortably afford, and other positive financial decisions. If you can clearly demonstrate you have adjusted your financial behaviour, then you might be able to find a lender who will loan you money.

It is worth highlighting here that if you are currently bankrupt – you are deemed as a high-risk borrower. In order to offset the high risk that you pose, lenders will typically only offer you loan options with very high interest rates, or loans that are secured to an asset. If you are unable to repay this loan, then you could put yourself under further financial strain.

Alternatives to taking on a personal loan

If you are currently in the bankruptcy process and in need of extra financial assistance, it might be a good idea to explore other alternatives as opposed to taking on more debt. This can include:

- Seeing if there is any government assistance available for you;

- Adjusting your lifestyle and cutting out any unnecessary expenses;

- Setting up a budget to get on top of your finances.

Can you get a personal loan after bankruptcy?

Now let’s tackle whether you can get a personal loan after bankruptcy. Once you have completed the bankruptcy process, there are no restrictions on applying for loans or credit. However, it is once again up to the credit provider to decide whether they will lend you money.

As we mentioned above, most credit providers will want to see evidence that you have improved your financial habits. This could include a solid banking history (not overdrawing your account, no direct debit reversals, etc.), no new defaults on your credit report and similar positive financial behaviour.

Your credit report will show your bankruptcy for either:

- 2 years from when your bankruptcy ends or;

- 5 years from the date you became bankrupt (whichever comes later).

Therefore, just because your bankruptcy has ended and you no longer have to inform lenders if you want a loan over $3,000, when they check your credit report, for two years after your bankruptcy has ended, they will be able to see that you were bankrupt.

Before you apply for any type of credit, it’s a good idea to check that you actually need it. Can you make some adjustments to your budget (or create a budget if you don’t have one), can you cut out any unnecessary expenses, or can you get government assistance to help you? These are some options you could consider.

While we at Tippla will always do our best to provide you with the information you need to financially thrive, it’s important to note that we’re not debt counsellors, nor do we provide financial advice. Be sure to speak to your financial services professional before making any decisions.