Bad Credit Loans | What Are They & How To Apply for Them

This text can be used to describe shortly what the Credit Score Basic is used for.

If you have a below-average credit score but you still want to take out a personal loan, what are your options? There is such a thing as bad credit loans. Tippla has provided a breakdown of bad credit loans below – what are they, the pros and cons of poor credit loans and how to apply for them.

What are bad credit loans?

As the name suggests, a bad credit loan is a loan you can take out when you have a “bad” credit score, also known as below average. The point of a bad credit personal loan is to allow people who don’t have a stellar credit history the opportunity to still access finance.

This can be helpful for people who need a loan but don’t have a great credit history and don’t have the time to improve their credit score.

Why does my credit score matter when applying for a loan?

Your credit score is a number ranging from 0 – 1,200 and it acts as an indicator of how reliable of a borrower you are. Your credit score is based on your recent credit history – your credit applications, your repayment history, the number of credit accounts you have, and any negative entries if applicable (defaults, bankruptcies, court judgements, etc).

Because of this, your credit score gives credit providers a helpful overview of how you have managed credit in the past. Lenders and banks use your credit score to judge how much of a risk you pose to them when you apply for some kind of credit, whether it be a loan, credit card, mortgage and more.

The higher your credit score, the more reliable of a borrower you are perceived to be. This can go a long way when it comes to applying for credit. This is because you’re more likely to be approved for a loan if you have a good credit score and positive credit history.

On the reverse side, if you have a bad credit score and a bad credit history, then your loan application might be rejected and credit because lenders will see you as too much of a risk.

What is a bad credit score?

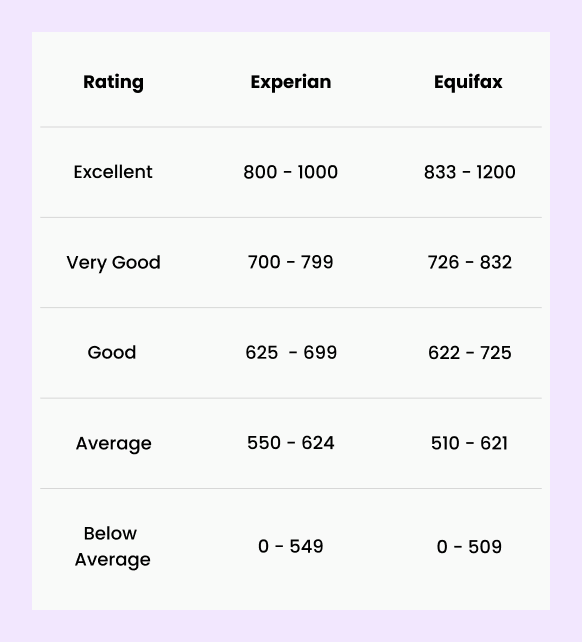

Your credit score will fall somewhere on a five-point scale: excellent, very good, good, average and below average. Below average is also referred to as a “bad” credit score.

Where your credit score falls will depend on the Credit Reporting Agency (CRA). In Australia, there are three CRAs – Equifax, Experian and illion. Each of these three agencies collects your credit information and generates your credit scores and reports. That means you have not one, but three credit scores and reports.

Equifax measures its credit scores on a scale from 0-1,200, whereas Experian and illion use a scale ranging from 0 – 1,000. Here’s how Equifax and Experian categorise their credit scores.

Source: Equifax and Experian

The pros and cons of bad credit loans

Are bad credit loans a good or a bad thing? Well, there are arguments for both sides. So let’s take a look at the pros and cons of bad credit loans.

Pros

1. Access to finance

One of the good things about bad credit loans is that it provides people who don’t have the best credit history with access to finance. Generally, the turnaround for these types of loans is quite fast, which can be helpful if you need cash quickly.

2. Can help you rebuild your credit

If you take out a loan, it can be your opportunity to rebuild your credit history. If you can make all of your repayments on time, and you can pay off the loan in full, these actions can both positively contribute to your credit score.

3. Extended repayment period

In Australia, you can get a range of bad credit loans, with varying repayment periods. This means you don’t have to pay back the amount you borrowed straight away, you can space out your repayments into affordable instalments.

Cons

1. High-interest rates

Lenders are taking on more of a risk by lending to people with a bad credit score. Because of this, they offset their losses with high-interest rates. Depending on where you go, you could be facing interest rates of up to 30% per annum in the most extreme cases.

The amount you pay in interest can add up over time, and it can hurt your wallet. You should make sure you can afford the repayments, including any interest and fees and charges, before taking on a loan.

2. Fees

Not only do bad credit loans come with higher interest rates, but they can also come with more fees. Again, this is a way for lenders to offset the risk of lending to someone with a bad credit score.

Just like interest, the amount you pay in fees can add up quickly if you’re not careful. That’s why it’s important to read the terms and conditions before taking on a loan.

3. Lower borrowing limits

Typically, if you have bad credit, then you might not be able to borrow as much as you’d like. This will differ from lender to lender, and you might find some that are willing to lend higher amounts, but again, you’ll likely be paying for this in interest and fees.

4. Collateral requirements

Some lenders may require you to offer some kind of collateral to take out a loan. If you default on the loan, then you could be at risk of losing your collateral.

Who offers bad credit loans?

Many lenders offer loans for people with bad credit. A simple google search for bad credit loans will produce pages of results of lenders who are willing to provide loans.

Typically speaking, you are more likely to find non-bank lenders who are willing to take on the added risk of lending to someone with bad credit.

How to apply for bad credit loans

Before applying for a loan, you should make sure you meet the criteria of the loan. In Australia, you will typically need to meet the following criteria:

- Be at least 18 years old;

- Be an Australian or New Zealand citizen (or Australian permanent resident/have an eligible Visa);

- Live in Australia;

- Be employed and receive a regular income.

You can apply for bad credit loans similar to how you would apply for any other loan, however, it is a good idea to do your research before applying. You should try and compare the different options out there, and see which lender can offer you the best conditions, such as interest rates and associated fees.

Bad credit loans: the verdict

To sum it all up, there are pros and cons to bad credit loans. If you are unsure if this type of loan is right for you, then you can reach out for free financial advice with a financial counsellor from the National Debt Helpline.

While we at Tippla will always do our best to provide you with the information you need to financially thrive, it’s important to note that we’re not debt counsellors, nor do we provide financial advice. Be sure to speak to your financial services professional before making any decisions.